1.1 Purpose

The pest control industry experienced steady top-line growth between 2023 and 2025. However, growth alone did not guarantee stronger profitability. Labor costs, indirect overhead, vehicle expenses, and growth-related investments have shifted differently across operators and company sizes. As a result, profitability increasingly depends not just on growth, but on how effectively operators manage their cost structure as they scale.

This study examines where profitability pressure is building within the pest control industry and how those pressures vary by revenue tier and operating model. By comparing performance across segmented peer groups, the benchmarks in this report help operators see where their business stands relative to industry norms and identify the operational drivers most responsible for Margin pressure.

Rather than relying on simple averages, the analysis focuses on performance distributions, highlighting the gap between median performance and best-quartile execution. Segmenting operators by revenue tier and region enables more meaningful comparisons that reflect differences in scale, labor markets, and operating environments. For example, operators generating less than $1M in revenue often face fundamentally different operational constraints than companies operating above $3M in annual revenue, where staffing structures, overhead allocation, and growth investments tend to evolve significantly.

The objective is not simply to measure performance, but to clarify the structural factors separating disciplined operators from those experiencing Margin compression heading into 2026. The analysis also highlights how operators achieving both strong growth and strong Margins manage these pressures differently, offering practical insights for businesses seeking to improve profitability without sacrificing growth.

FRAXN's role is to translate financial data into clear, consistent reporting structures that reflect how the business has actually performed. This includes analyzing what the levers behind those numbers are, identifying where performance is stable or volatile, and clarifying what the data supports today. The objective is not to prescribe actions, but to make the financials transparent and defensible so operators can make informed decisions grounded in reality.

1.2 Who Should Read This Report

This study is most relevant for decision-makers within pest control organizations, including:

- Owners and founder-operators

- General managers and COOs

- CFOs and finance leaders

- Growth-focused operators evaluating operational scalability

- Investors and strategic partners (secondary audience)

The analysis is particularly useful for operators seeking to:

- Benchmark cost structure against similarly sized peers

- Diagnose Margin compression despite Revenue Growth

- Evaluate whether growth investment is translating into profitable expansion

- Inform 2026 planning with realistic, scale-adjusted financial guardrails

- This report is not intended as a general industry overview. It is a structural benchmarking study designed for operators actively managing cost discipline, growth quality, and long-term profitability.

1.3 What Makes This Study Different

Unlike traditional industry surveys that rely on blended averages, this study emphasizes structural dispersion, meaningful segmentation, and multi-year performance trends.

Key differentiators include:

- Segmentation FirstBenchmarks are presented by revenue tier and region, avoiding blended averages that can obscure the operational dynamics of scale.

- Multi-Year PerspectiveLeveraging full-year financial data from 60 operators, the study provides a multi-year comparison spanning 2023–2025, highlighting how performance patterns evolve over time.

- Distribution-Based MetricsResults are reported using medians and quartile ranges rather than simple averages. This approach reduces distortion from outliers and provides a clearer picture of typical operator performance.

- Dynamic Performance AnalysisBeyond static benchmarks, the study introduces performance relationship analysis, examining how key variables interact rather than viewing them in isolation. Visual analyses such as Revenue Growth versus expense expansion, growth versus Margin change, and investment intensity versus profitability highlight the structural trade-offs operators face when scaling. These relationship-based insights reveal patterns that traditional quartile tables alone cannot capture.

- Growth Quality FrameworkThe study evaluates not only how fast operators grow, but also how efficiently they grow. By examining how expenses scale relative to revenue, the analysis links cost behavior directly to EBITDA outcomes. This approach helps operators understand not just where they stand, but why performance differs across the industry and how those differences evolve over time.

tldr; Chapter 1 — Report Positioning

Summary Points

- This report exists because revenue growth alone doesn't tell you enough.Between 2023 and 2025, most pest control operators grew. But labor costs, indirect overhead, and vehicle expenses quietly eroded margins for many of them. Knowing your revenue number is not the same as knowing how your business is actually performing.

- The data comes from real financials, not surveys.Every figure in this study is drawn from actual bookkeeping records, standardized into a consistent framework across 125 operators. That is what makes it useful. Industry surveys measure what operators believe. This report measures what their books actually show.

- The goal is practical, not academic.This report is designed to answer four questions: Where is margin pressure building? How does your performance compare to peers? Which cost drivers separate disciplined operators from the rest? And what financial guardrails should shape your 2026 planning?

- This report is for you if you have ever looked at your P&L and thought, "I'm not sure if this is good or not."Whether you grew and want to know if your margins kept pace, or you're preparing for 2026 and want data-backed benchmarks, this report was built to answer those questions with real numbers, not industry generalizations.

- How to use it: find your tier, match your region, compare to median and top quartile.Use your 2025 revenue to identify your tier (under $1M, $1M to $3M, $3M+). Reference your region for additional context. Then focus on the largest gap between your numbers and the top quartile, and start there.

- Median is not the goal. Understanding why the gap exists is.The most valuable part of benchmarking is not the number itself. It is the question it forces: why does my business look different from the most disciplined operators, and what cost decisions are driving that difference?

See How Your Numbers Compare

Every benchmark in this report can be applied directly to your own P&L. If you want to know exactly where your business stands, FRAXN works with pest control operators to build the financial clarity this report measures. Visit fraxn.com or scan the QR code to learn more.

2.1 Data Source and Standardization

This study is built from operator-level financial data provided by participating pest control companies. To ensure comparability across businesses with different bookkeeping practices, financial entries were standardized into a consistent chart-of-accounts (COA) structure, enabling true apples-to-apples benchmarking.

Because accounting treatment varies across operators, particularly for subcontracted labor, fleet costs, and employee-related expenses, accounts are mapped based on economic function rather than company-specific chart-of-accounts structures. For example, indirect payroll is separated to exclude compensation attributable to Sales and Marketing activities when those costs are recorded within broader payroll accounts. This ensures benchmarks reflect operational reality rather than accounting classification differences.

2.2 Cohort Definition

Two cohorts are referenced throughout this study:

- Cohort A (3-Year Trend Cohort):Operators with complete financial data for 2023–2025 (n = 60). This cohort is used exclusively for multi-year trend analysis and volatility insights. It represents a subset of the broader benchmark sample.

- Cohort B (Benchmark Cohort):Operators with complete financial data for 2024–2025 (n = 125) comprise the primary benchmarking cohort used for cost structure analysis, segmentation, growth comparisons, and profitability evaluation. Within this group, nine operators began operations partway through 2024. Although these companies report financial data for both years, their 2024 results do not represent a full operating period.

To preserve true comparability and avoid distortion from partial-year ramp-up effects, FRAXN did not annualize their 2024 financial records to account for missing months. Where full-year comparability is required for 2024–2025 analysis, the study uses a subset of operators with complete operating periods, referred to as the comparable cohort (n = 116). The full benchmark cohort (n = 125) is retained for structural benchmarking analyses. Unless otherwise noted, all structural benchmarking results reference Cohort B (n = 125).

2.3 Chart of Accounts to Benchmark Mapping

Each operator's financials have been translated into FRAXN's uniform chart of accounts providing a standardized benchmarking framework. A full chart-of-accounts (COA) mapping used in this study is provided in the Appendix for reference.

The guiding principle is straightforward:

- Cost of Service (COS)reflects what it takes to perform the work.

- Operating Expense (OPEX)reflects what it takes to run and grow the company.

Unless otherwise noted, benchmarks are expressed as a percentage of revenue for the applicable year of analysis.

Year-over-year changes in cost structure are measured as percentage-point (pp) differences relative to revenue, not as dollar growth rates. For example, if Cost of Service increases from 45% of revenue in 2024 to 48% in 2025, the change is reported as a +3 percentage-point increase, meaning $0.48 of every revenue dollar is now spent performing the work, compared with $0.45 the prior year.

Comparative revenue tiers are based on 2024 baseline revenue and remain fixed across the 2023–2024 and 2024–2025 comparisons to avoid artificial tier migration.

2.4 Benchmark Statistics and Weighting

All published benchmarks use company-weighted distribution statistics:

- Median (50th percentile)

- Best Quartile (75th or 25th percentile depending on the benchmarking metric)

Company-weighted means each operator contributes equally to the distribution, regardless of company size or revenue scale.

Because benchmarks rely on medians and quartiles rather than arithmetic averages, extreme values have reduced influence on the published statistics. Observations are retained unless a clear data integrity issue is identified.

Distribution statistics are used instead of revenue-weighted averages to preserve comparability across operators of different sizes and operating scales.

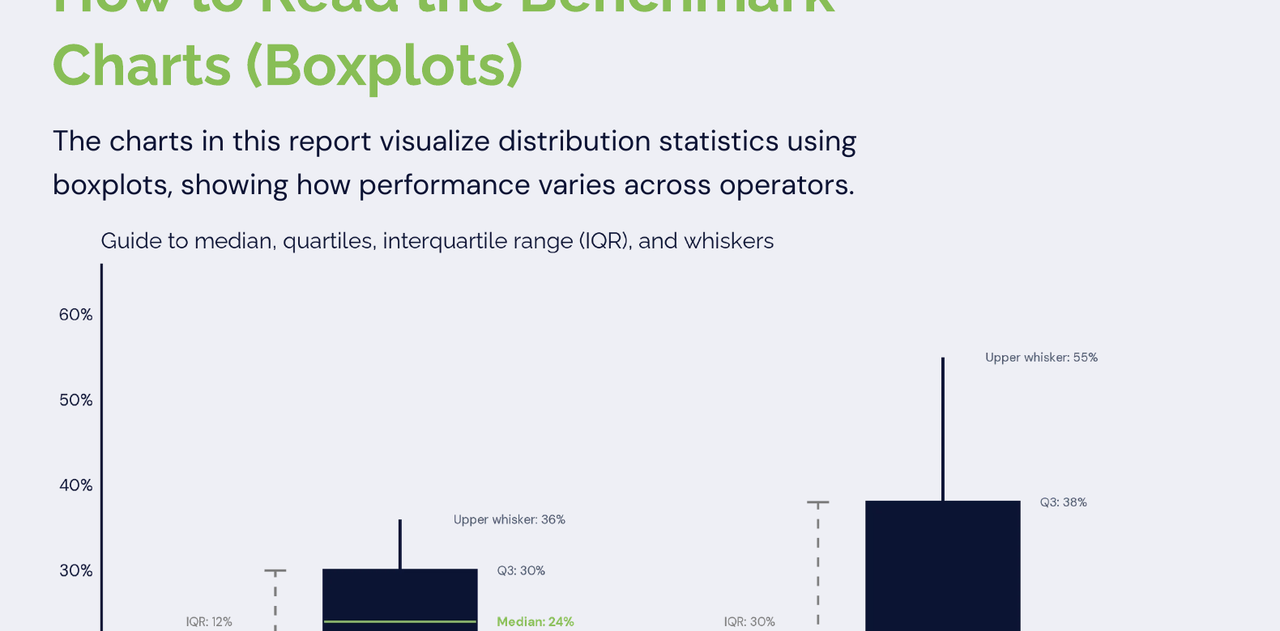

How to Read the Benchmark Charts (Boxplots)

The charts in this report visualize distribution statistics using boxplots, showing how performance varies across operators.

Each boxplot summarizes the distribution:

- The horizontal line inside the box represents the median, which is the typical operator performance.

- The box shows the distribution of the middle 50% of operators. Where the upper edge represents the Q3 (75th percentile) while the lower edge represents Q1 (25th percentile).

- The height of the box (IQR) reflects how consistent or variable the results of the middle 50% are across peers.

- The whiskers show how far results extend beyond the middle 50% of operators, indicating the wider range of outcomes in the dataset.

How to interpret the Distribution:

The example chart above illustrates how distributions can differ even when medians are similar.

- In the tighter spread example, results are more consistent:

- Median: 24%

- Most operators fall within a narrow range (18% to 30%)

- The IQR is relatively small (12 percentage points gap)

- In the wider spread example, performance varies significantly:

- Median: 22% (similar to the first example)

- However, results range much more widely (6% to 38% within the box)

- The IQR spreads to 30 percentage points, indicating higher variability

Despite having similar median values, the second group shows much greater dispersion, meaning operator performance is less consistent and more diverse. On this example you can initially ask the "Same median = same performance environment".

How to Benchmark Yourself

Use each chart to assess your position:

- At the median = You are in line with the typical operator

- Above or below the median = You are outperforming or lagging peers

- Outside the box (above Q3 or below Q1) = You are materially different from the market

- Within the box = You are operating within the typical range

Interpreting "Best Quartile"

"Best" performance depends on the metric:

- Growth and profitability metrics → Higher is better (top quartile / Q3)

- Expense metrics → Lower is better (bottom quartile / Q1)

What to Focus On

When reviewing benchmarks, focus on:

- Your distance from the median

- The spread of the distribution (tight vs wide)

- Which cost or revenue drivers explain the gap

Benchmarking your operating figures shows where you stand while the distribution shows how competitive that position really is.

2.5 Metric Construction — Core Benchmark KPIs

Profitability in this report is evaluated through a sequential operating structure that reflects how revenue converts into operating profit. The benchmarks follow a simple progression:

Revenue → Cost of Service → Gross Margin →

→ Operating Expenses → EBITDA Margin %

This structure isolates where Margin pressure originates, whether within service delivery or within broader operating overhead.

Revenue and Profitability Benchmarks

The following metrics capture the primary performance outcomes of pest control operators, including Revenue Growth, Gross Margin, and operating profitability. These benchmarks reflect how effectively operators convert revenue into profit across different cost structures and operating models.

Revenue Growth %

(Current Year Revenue − Prior Year Revenue) ÷ Prior Year Revenue

Measures year-over-year change in total revenue relative to the prior-year baseline. Revenue Growth reflects the pace at which operators expand through customer acquisition, pricing adjustments, and service volume.

Gross Margin %

(Revenue − Cost of Service) ÷ Revenue

Measures the portion of revenue remaining after direct service delivery costs are deducted.

Gross Margin provides an indicator of field-level operating efficiency before administrative overhead and growth investments are considered. It helps determine whether Margin pressure originates within service delivery or elsewhere in the cost structure.

EBITDA Margin %

(Revenue − Cost of Service − Operating Expenses) ÷ Revenue

Measures overall operating profitability after both service delivery costs and operating overhead are deducted.

For benchmarking consistency, accounts related to financing activities, income taxes, and other non-operating items are excluded from the analysis.

Because depreciation, amortization, and certain non-operating accounts are not consistently reported across operators, EBITDA in this study should be interpreted as an operating profitability benchmark rather than a strict accounting EBITDA measure.

This standardized definition provides a consistent basis for comparison across operators regardless of capital structure, ownership, or accounting treatment.

Cost Benchmarks

The following metrics decompose the operating cost structure underlying Gross Margin and operating profitability. Evaluating each component individually reveals the cost drivers behind the performance benchmarks.

Cost of Service (COS) %

Cost of Service ÷ Revenue

Cost of Service includes only direct costs required to deliver pest control services, including:

- Direct Field Labor ExpenseIncludes Payroll, payroll taxes, benefits, and subcontractor payments for technicians and other personnel directly performing field service work.

- Materials, Chemicals & Small Equipment Expenseincludes operating inputs directly consumed in the delivery of pest control services, including chemicals and treatment products; baits, traps, and other consumable supplies; small tools and service equipment purchases; equipment leases directly tied to field operations; and field uniforms and related service gear.

- Direct Field Vehicle / Fleet Expenseincludes fleet-related costs directly tied to service delivery, such as fuel, lease, repairs, maintenance, insurance and other vehicle expenses.

Note: Where operators record vehicle costs across multiple accounts, expenses are mapped based on their economic function to ensure costs associated with field service delivery are consistently included in Cost of Service.

- Other Direct Costincludes other expenses that are directly attributable to performing field work.

Operating Expenses (OPEX) %

Operating Expenses ÷ Revenue

Operating Expenses represent all indirect costs required to support the business beyond direct service delivery.

OPEX is not benchmarked as a single aggregate percentage in this study. Instead, analysis is performed at the component level to improve diagnostic precision and allow operators to isolate specific cost drivers rather than reacting to blended overhead totals.

Primary OPEX components include:

- Indirect Labor Expenseincludes personnel-related expenses for non-field roles that support operations, administration, and management functions.

Note: Where payroll accounts combine multiple functions, compensation is reclassified based on job function to ensure administrative labor is separated from field labor and Sales & Marketing activities.

- Sales & Marketingincludes all payroll and non-payroll expenses directly associated with customer acquisition, promotion, and revenue generation. Sales & Marketing % reflects customer acquisition intensity and growth investment level. It should be evaluated alongside Revenue Growth %, Gross Margin %, and payback metrics when assessing growth efficiency.

Note: Where sales-related payroll or marketing expenses are embedded within broader payroll or administrative accounts, costs are mapped to Sales & Marketing based on their underlying economic function.

- Facility / Occupancyincludes all costs associated with maintaining office, warehouse, and operational premises, as well as supporting communication and office infrastructure.

- G&Aincludes corporate-level administrative, financial, compliance, insurance, professional service, and general business expenses required to manage and govern the company that are not directly tied to service delivery, fleet operations, sales and marketing, or facility infrastructure.

- Other Indirect Costincludes other expenses required to support the business beyond direct service delivery.

Note on Interpretation: All cost metrics are expressed as a percentage of revenue at the company level and summarized using the median across operators. Because each component is calculated and aggregated independently, the sum of median cost components will not equal total Cost of Service or Operating Expenses and will not reconcile to 100%.

This approach is intentional and provides a more accurate view of typical cost allocation across operators, avoiding distortion from outliers or differences in company size.

2.6 Segmentation Approach

Benchmarks are segmented to avoid blended averages that may obscure scale effects.

Primary segmentation: Revenue Tier (based on annualized revenue)

After careful consideration and participant analysis, FRAXN categorized participants into three revenue segments based on their annualized revenue.

- Less than $1M (<$1M)Those operators with less than $1M annualized revenue.

- $1M to $3M ($1M−$3M)Those operators with revenues between $1M and $3M annualized revenue.

- Greater than $3M ($3M+)Those operators with revenue greater than $3M annualized revenue.

For a more detailed overview of participant distribution by Revenue Tiers, please refer to Chapter 4.2 Revenue Tier Distribution.

Secondary segmentation: Region (where sample sizes support meaningful comparison)

Operators should benchmark primarily against their revenue tier and then reference regional comparisons where applicable.

The regions included in this report are:

Mid-Atlantic North Central North East Pacific North West

South Central South East South West

For a more detailed overview of participant distribution by Region, including state-level representation, please refer to Chapter 4.3 Geographic Representation.

2.7 Data Limitations

Regional Coverage

Cohort A (2023–2025 trend cohort) has limited participation in certain regions. No North Central operators currently meet full three-year data requirements. As a result, three-year trend analysis for that region is not presented.

In regions with smaller sample sizes, benchmark results should be interpreted with appropriate caution, as thinner cohorts may be more sensitive to the performance of a small number of operators. As participation expands over time, regional benchmarks are expected to become more stable and representative.

Scale Sensitivity in <$1M Tier

Within the <$1M revenue tier, percentage changes in growth and Margin metrics may appear amplified due to smaller revenue bases. These observations are retained in the dataset. However, the use of company-weighted medians and quartiles reduces the influence of extreme values. Results should be interpreted with appropriate consideration of scale sensitivity.

Source Data Treatment

Financial data used in this study is derived from a combination of operator-submitted bookkeeping records and FRAXN-managed accounting records. While FRAXN standardizes accounts into a consistent benchmarking framework, underlying transaction classification generally follows each participating company's internal reporting practices.

FRAXN performs structural mapping to a standardized chart-of-accounts to ensure comparability across operators. However, no forensic reclassification, audit procedures, or reconstruction of financial statements were performed beyond this standardization process.

As a result, the benchmarks presented in this report reflect reported operating performance rather than audited or restated financial results.

Treatment of Negative Category Totals

Negative totals within Cost of Service (COS) or Operating Expense (OPEX) categories may occur due to accounting reversals, reclassifications, or one-time adjustments. Immaterial negative amounts are retained. Where negative category totals exceed a materiality threshold (e.g., 1% of revenue), they are capped at zero for benchmarking ratio calculations to preserve structural comparability across operators.

Visualization Adjustments

In certain visualizations, particularly scatter plots, extreme outlier observations may be omitted from the chart display to improve readability and highlight the primary distribution of results. These extreme cases represent a very small number of observations and do not materially affect the underlying benchmark calculations.

Unless otherwise noted, distribution statistics and benchmark values are calculated using the full dataset, with observations retained unless a clear data integrity issue is identified.

Go-to-Market Model Differences (D2D / High Acquisition Spend)

Some operators utilize door-to-door (D2D) or other high-investment sales models, which structurally increase sales payroll and marketing expense relative to peers. Benchmark comparisons should account for differences in go-to-market strategy, customer acquisition intensity, and service mix when interpreting cost structure and Margin outcomes. Results should be interpreted with appropriate consideration of this business model differences.

tldr; Chapter 2 — Data, Cohorts, and Methodology

Summary Points

- Two cohorts. One for benchmarking, one for trends. Cohort B is 125 operators with complete 2024 and 2025 financials, used for all primary benchmarks. Cohort A is a 60-operator subset with three full years of data (2023 to 2025), used exclusively for multi-year trend analysis. These are not interchangeable.

- Every operator's financials were standardized before any comparison was made. Businesses with different bookkeeping practices, account structures, and expense classifications are translated into a consistent chart of accounts before a single benchmark is calculated. This is what makes the numbers comparable.

- Cost of Service covers what it takes to perform the work. Direct Field Labor, materials and chemicals, and field vehicles. Operating Expenses cover what it takes to run and grow the company: indirect labor, Sales and Marketing, facility costs, and G&A. Understanding which side of that line your costs live on is the foundation of this entire analysis.

- Medians and quartile ranges, not averages. This prevents a handful of unusually large or small operators from skewing the results. Every operator contributes equally to the distribution regardless of company size. When you see a benchmark number in this report, it represents the typical operator, not an outlier-influenced mean.

- Benchmarks are segmented by revenue tier and region. Comparing a $500K operator to a $5M operator produces noise, not insight. Tier and region segmentation ensures you are always looking at peers operating under similar conditions. Always use your revenue tier before layering in regional context.

- Door-to-door and high-acquisition models will look different. If your go-to-market relies on D2D sales or aggressive acquisition spend, your Sales and Marketing costs will structurally sit above the benchmark median. That is not a red flag. It reflects a deliberate strategy, and the report accounts for that distinction.

- The data reflects reported operating performance, not audited financials. Accounts are standardized for comparability. They are not reconstructed or restated. That distinction matters when interpreting any benchmark figure and is documented in full in the methodology appendix.

Industry Performance Snapshot

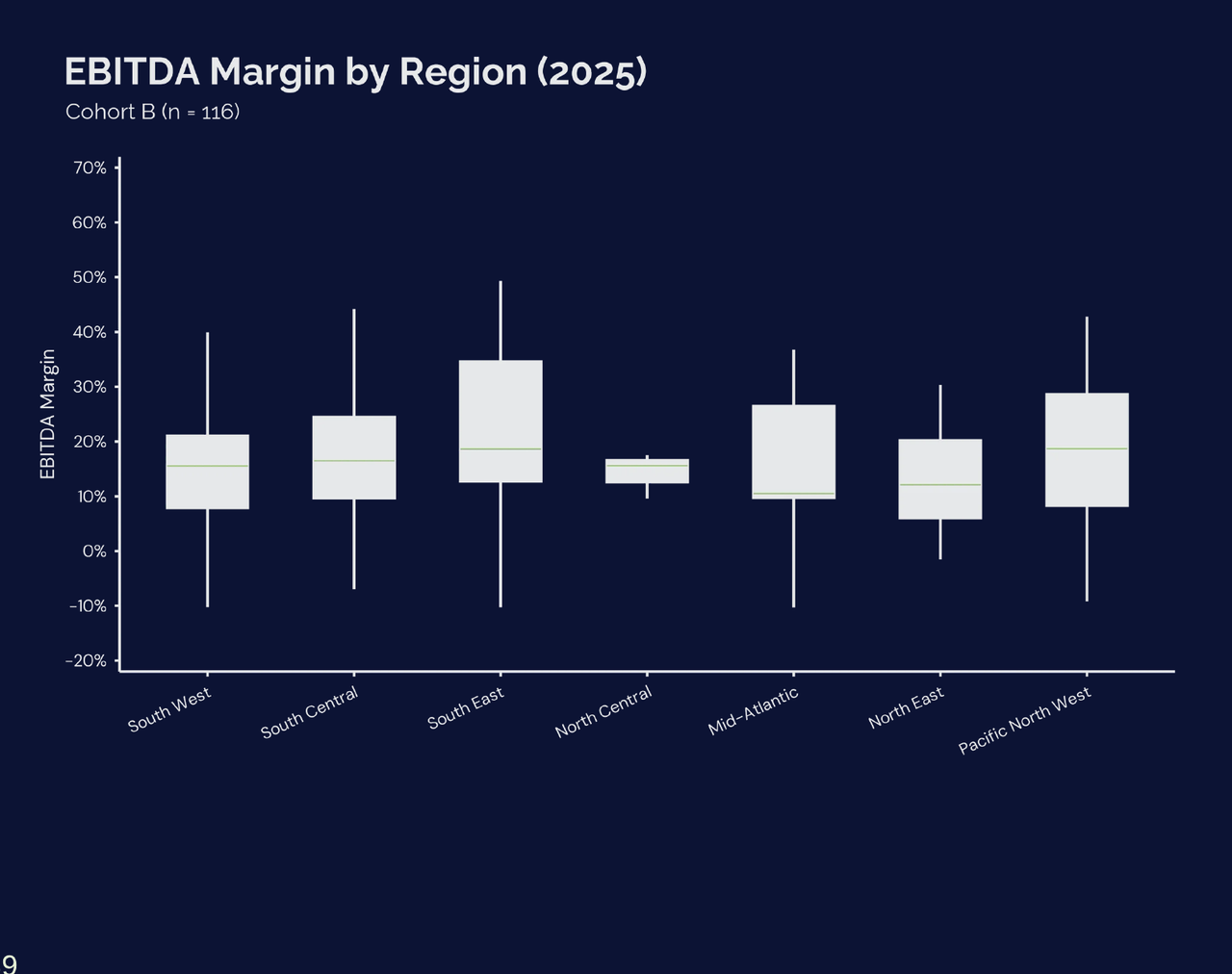

This benchmark study analyzes financial performance across 125 pest control operators, with 116 companies forming the comparable cohort used for growth and profitability analysis between 2024 and 2025. Participating operators span multiple revenue tiers and geographic regions, providing a broad view of the economic structure of modern pest control businesses.

At a structural level, the economics of pest-control operators demonstrates a consistent, cost-intensive model across all revenue tiers.

Across the benchmark cohort:

- Cost of Service represents approximately 35–40% of revenue

- Operating Expenses account for roughly 44–46% of revenue

- Resulting in median EBITDA Margins of 15–17%

While larger operators benefit from higher Gross Margins, this advantage is partially offset by higher overhead requirements, resulting in relatively similar EBITDA Margins across tiers. This highlights that scale alone does not guarantee improved profitability and cost discipline remains critical at all levels.

Overall, the industry continues to demonstrate strong expansion. Median Revenue Growth reached 15.4%, with the middle 50% of operators growing between 5.7% and 28.9%. This reflects sustained demand for recurring pest management services and continued expansion across many operators.

However, Revenue Growth did not consistently translate into stronger profitability. For many operators, expenses increased at a similar or faster rate than revenue, limiting Margin expansion.

These findings indicate that the next phase of industry performance will depend less on pure Revenue Growth and more on how effectively operators manage cost components such as labor productivity, marketing efficiency, and overhead structure as they scale.

Growth Remains Strong, but Expenses Are Expanding at Similar Rates

A consistent pattern across the study is the close relationship between Revenue Growth and Expense Growth.

Many operators cluster near the diagonal line, where revenue and expenses are growing at similar rates. Points above this line represent companies whose total costs and expenses are rising faster than revenue, placing pressure on margins. Points below the line indicate operators that are successfully capturing operating leverage, where revenue growth outpaces growth in costs and expenses. Of the 116 operators analyzed, 56 experienced Expense Growth outpacing revenue, while 60 achieved Revenue Growth ahead of expenses, representing a near-even split between less efficient and more efficient growth outcomes.

While some companies achieved strong growth alongside improving margins, the broader distribution shows that growth alone does not guarantee stronger profitability. Expansion often requires reinvestment in technician capacity, marketing, and operational infrastructure. Operators that convert growth into margin improvement tend to maintain discipline in staffing, route density, and marketing efficiency.

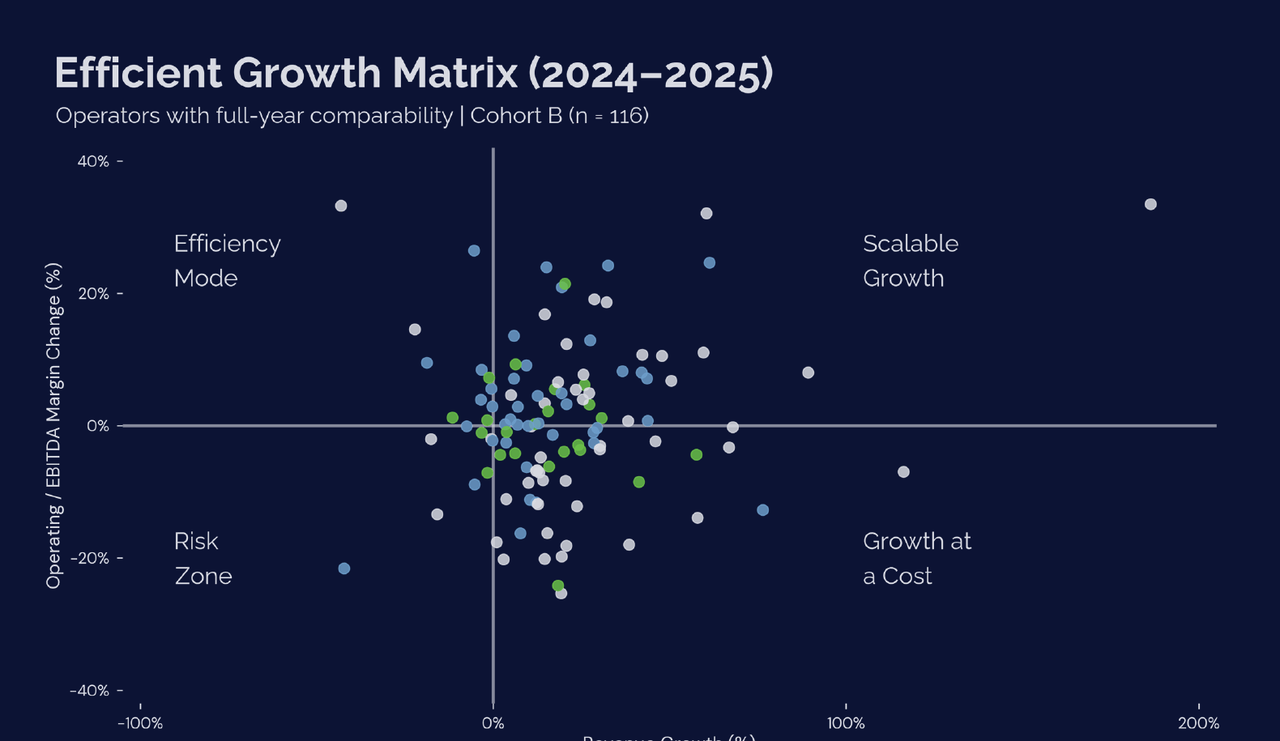

Efficient Growth Is Not Universal

The relationship between Revenue Growth and Margin change reveals four distinct operating profiles among the 116 operators with full-year comparability.

| Quadrant | Operators (n) | Share of Sample | Median Revenue Growth | Median EBITDA Margin Change |

|---|---|---|---|---|

| Scalable Growth | 49 | 42% | 23.4% | +7.1% |

| Growth at a Cost | 47 | 41% | 16.8% | -6.8% |

| Efficiency Mode | 11 | 9% | -3.5% | +7.3% |

| Risk Zone | 9 | 8% | -5.2% | -2.2% |

- Scalable Growth | upper-right quadrant:Strong Revenue Growth with improving Margins

- Growth at a Cost | lower-right quadrant:Revenue Growth accompanied by Margin compression

- Efficiency Mode | upper-left quadrant:Stable profitability with slower growth

- Risk Zone | lower-left quadrant:Declining growth and Margins

The distribution across these profiles reinforces a key finding: efficient growth is not universal. While 42% of operators achieved both revenue expansion and margin improvement, nearly equally 41% grew revenue at the expense of maximized profitability.

Note: not all "Growth at a Cost" outcomes are equally negative. While 33 operators in this quadrant experienced a decline in absolute EBITDA dollar value, 14 operators (30%) still increased EBITDA despite margin compression. This indicates that in some cases, revenue growth was sufficient to offset declining margins, resulting in higher absolute profit even as efficiency weakened.

Only 17% of operators experienced revenue contraction, indicating that the industry broadly expanded during the period. Notably, over 80% of companies increased revenue, but nearly half did so without improving profitability.

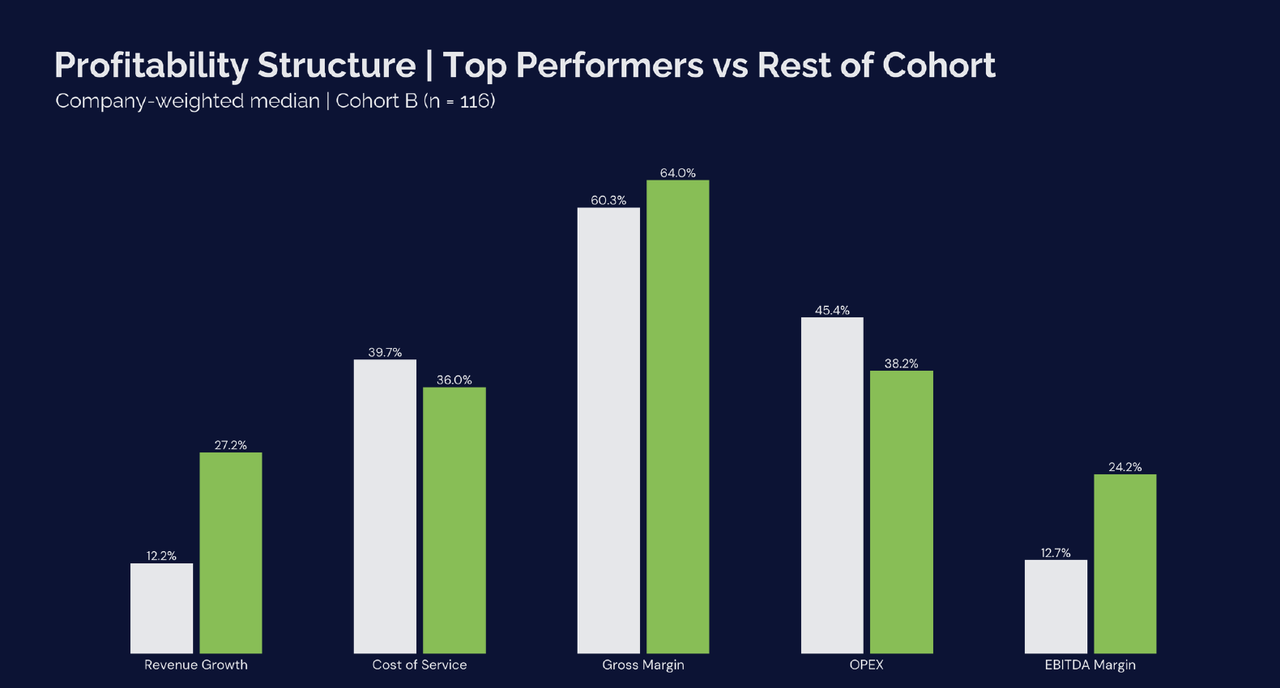

What Separates Top Performers

Operators achieving both above-median growth and profitability share several consistent characteristics.

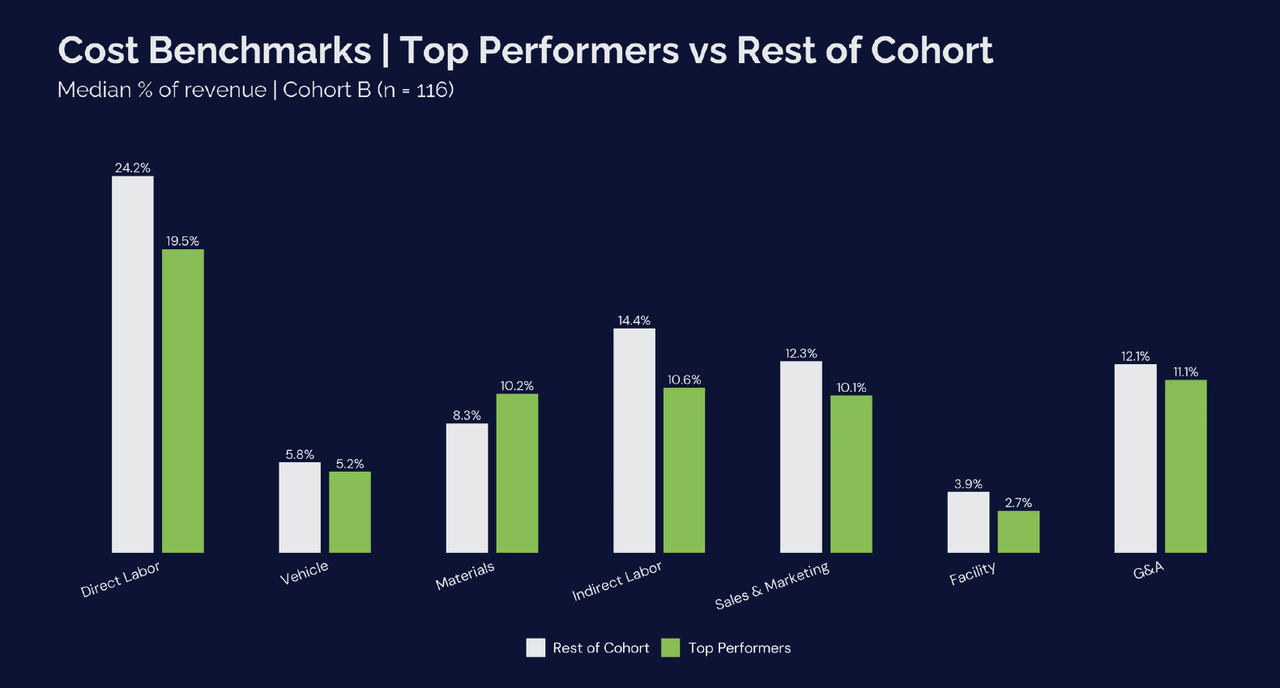

Top performers maintain lower Cost of Service ratios, indicating stronger technician productivity and more efficient service delivery. They also operate with leaner staffing structures, resulting in lower overall people costs.

At a more diagnostic level, the cost structure reveals a clear pattern. Top performers maintain leaner benchmarks across all OPEX components. However, within Cost of Service, a different trend emerges. Top performers allocate a higher share of revenue to Materials, Chemicals, Equipment, and Field Supplies (10.2% vs 8.3%), signaling a deliberate investment in service quality rather than aggressive cost minimization. In the context of pest control, where outcomes are directly tied to treatment effectiveness, this higher spend likely supports better customer retention, fewer callbacks, and stronger recurring revenue streams.

Unlike labor or overhead, materials and equipment represent a critical input to service quality, not just a cost line to optimize. Underinvestment in chemicals or application equipment can compromise treatment effectiveness, leading to reduced customer satisfaction and higher churn, ultimately eroding long-term profitability.

Top performers demonstrate that growth and profitability are not mutually exclusive — they are the result of disciplined execution across labor, service delivery expenses, pricing, and operational structure.

Planning Implications for Operators

Several practical implications emerge from the benchmark analysis:

- Growth remains achievable but requires reinvestment Expansion typically requires increased spending in labor, marketing, and higher-quality service delivery inputs.

- Labor productivity is the primary profitability driver Improvements in technician efficiency and route density have a direct impact on Margins.

- Marketing effectiveness matters more than scale Successful operators focus on conversion and payback rather than increasing spend alone.

- Overhead discipline becomes critical at scale As companies grow, controlling administrative and support costs is essential to maintaining profitability.

tldr; Chapter 3 — Executive Summary

Summary Points

- The industry grew.Median Revenue Growth across 125 operators was 15.4% in 2025, with the middle 50% landing between 5.7% and 28.9%. Demand for pest control services remains strong and broadly distributed across regions and company sizes.

- Revenue growth did not reliably become profit.For many operators, expenses grew at roughly the same rate as revenue. The result: EBITDA Margins were essentially flat at the median, hovering between 15% and 17% across all revenue tiers.

- Scale did not solve the problem.Larger operators ($3M+) achieved higher Gross Margins from better route density and technician efficiency. Those gains were almost entirely offset by heavier overhead. Median EBITDA Margins were similar across every tier.

- Growth quality varied sharply.42% of operators achieved scalable growth (revenue up, margins up). 41% grew revenue while margins declined. Only 17% experienced any revenue contraction, meaning most of the industry is growing, but nearly half are growing at a cost.

- Top performers play a different game.Operators achieving both above-median growth and above-median profitability maintained lower labor costs, leaner overhead, and more efficient marketing. They also spent more on materials and chemicals, not less. Service quality drives retention.

- The next competitive edge is cost discipline.The pest control industry has captured the growth. The operators who build lasting businesses will be the ones who manage what it costs to deliver and support that growth.

Are You Growing Efficiently or Just Growing?

The benchmark shows clearly that revenue growth and profitability are two different things. FRAXN helps pest control operators track the metrics that answer that question every single month. Visit fraxn.com or scan the QR code to learn more.

4.1 Cohort Composition

The benchmark dataset (Cohort B) includes 125 operators with complete financial data for 2024–2025, forming the primary benchmarking cohort used throughout the study. Nine operators began reporting financial data mid-year in 2024. While these operators are included in the benchmark cohort for structural cost comparisons, they are excluded from 2024–2025 comparative analysis (n=116) to ensure full-year comparability. Revenue figures were not annualized to avoid distortion from ramp-up periods.

A subset of 60 operators with complete financial data from 2023–2025 (Cohort A) forms the trend cohort, which is used for multi-year growth and volatility analysis.

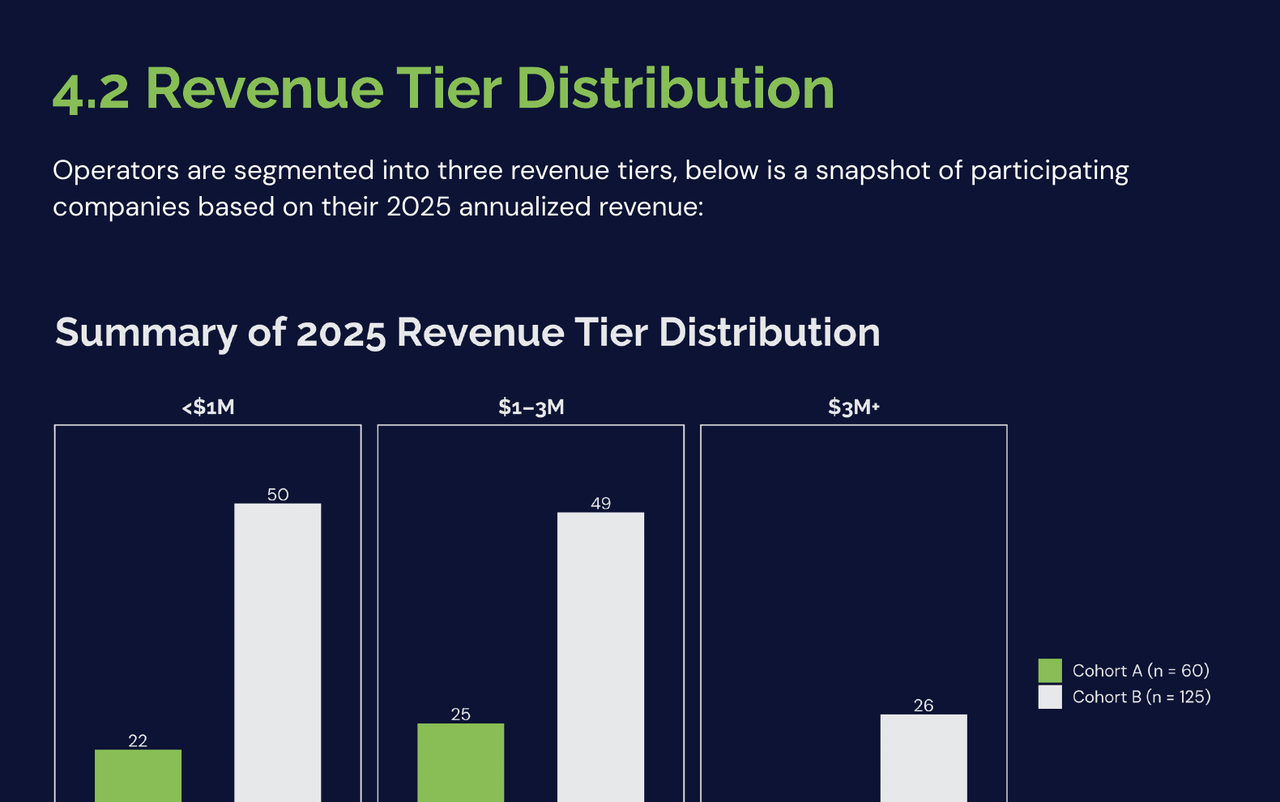

4.2 Revenue Tier Distribution

Operators are segmented into three revenue tiers, below is a snapshot of participating companies based on their 2025 annualized revenue:

Benchmark tables use 2025 tier placement. Multi-year trend analysis uses a fixed baseline year 2024 to avoid artificial "tier jumping" caused by rapid growth.

Operators should first benchmark themselves against peers within the same revenue tier, as cost structure, staffing models, and overhead leverage tend to change materially as companies scale. Smaller operators typically rely on lean technician-driven operations, while larger operators often carry additional management layers, sales infrastructure, and administrative support. Comparing performance within similar revenue tiers helps ensure that benchmarking reflects structural differences rather than scale effects.

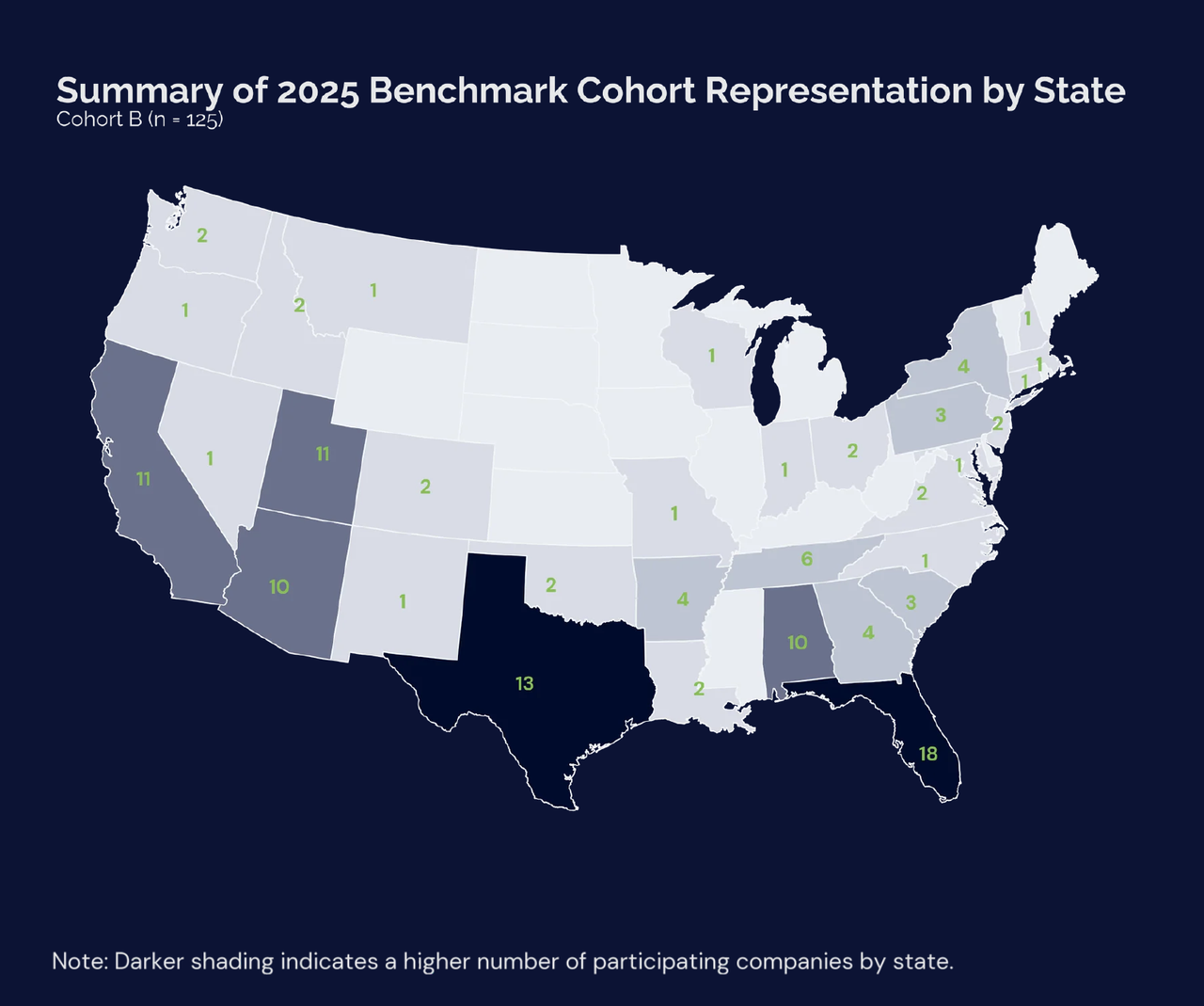

4.3 Geographic Representation

Participating operators span seven U.S. regions, providing broad geographic representation across diverse labor markets, service environments, and pricing conditions. In total, the benchmark cohort includes 125 companies distributed across these regions, with representation concentrated in the South East, South West, and South Central markets.

The regional composition and number of participating operators per state in this report is as follows:

- Mid-Atlantic (n = 10)Maryland (1), North Carolina (1), Tennessee (6), Virginia (2)

- North Central (n = 4)Indiana (1), Ohio (2), Wisconsin (1)

- North East (n = 12)Connecticut (1), Massachusetts (1), New Hampshire (1), New Jersey (2), New York (4), Pennsylvania (3)

- Pacific North West (n = 6)Idaho (2), Montana (1), Oregon (1), Washington (2)

- South Central (n = 25)Arkansas (4), Colorado (2), Louisiana (2), Missouri (1), New Mexico (1), Oklahoma (2), Texas (13)

- South East (n = 35)Alabama (10), Florida (18), Georgia (4), South Carolina (3)

- South West (n = 33)Arizona (10), California (11), Nevada (1), Utah (11)

Regional segmentation is applied where sample sizes support statistically meaningful comparisons, enabling operators to benchmark performance against peers operating under similar structural conditions.

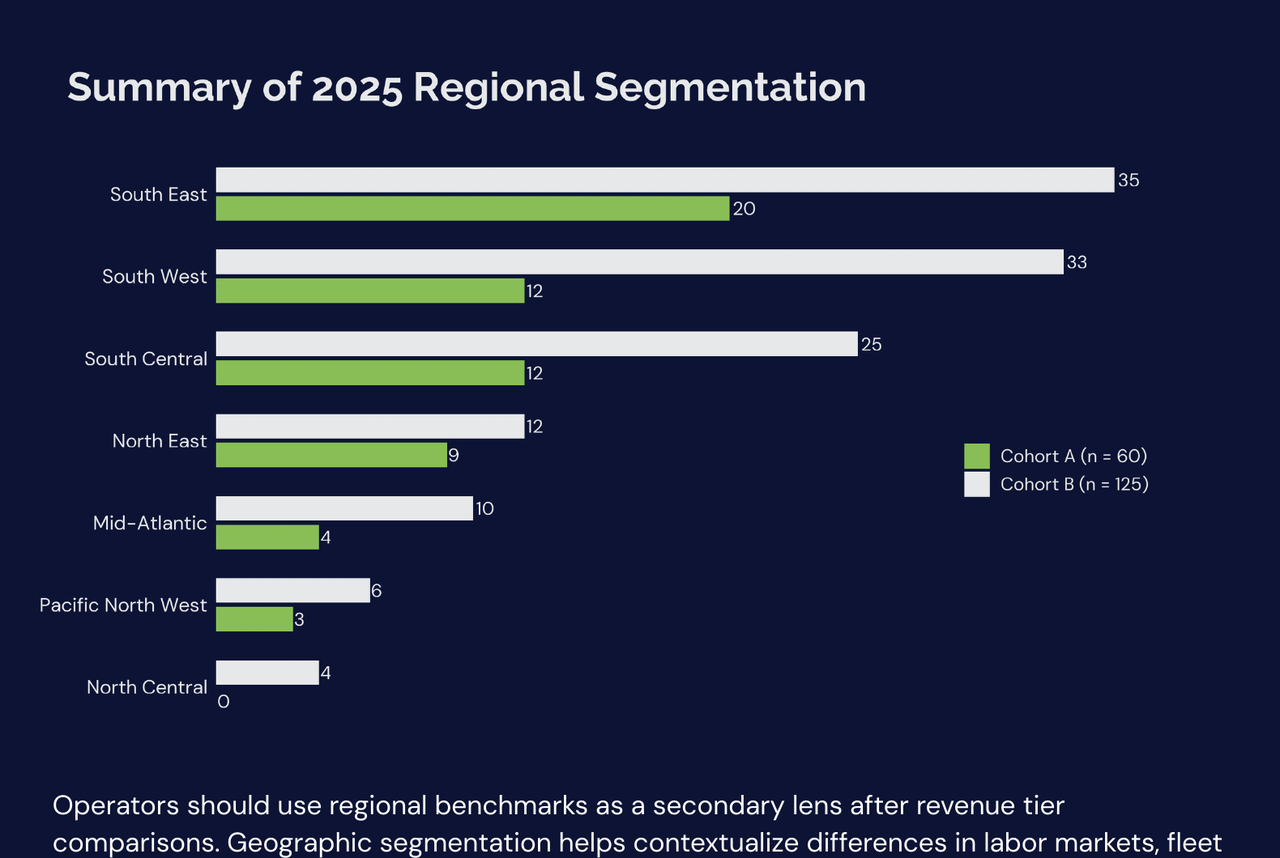

The chart below summarizes regional participation across both cohorts, with 60 operators in the three-year trend cohort (Cohort A) and 125 operators in the benchmark cohort (Cohort B). Regions with smaller sample sizes, particularly North Central and Pacific North West, should be interpreted with appropriate caution, as results may be more sensitive to individual operator performance.

Operators should use regional benchmarks as a secondary lens after revenue tier comparisons. Geographic segmentation helps contextualize differences in labor markets, fleet operating costs, pricing dynamics, competition intensity, and service mix across regions. Benchmarking against peers operating in similar environments helps distinguish structural cost differences from internal operational inefficiencies.

tldr; Chapter 4 — Benchmark Dataset Overview

Summary Points

- 125 operators form the primary benchmark cohort. These are companies with complete financial data for 2024 and 2025. A separate 60-operator subset with three full years of data (2023 to 2025) is used exclusively for multi-year trend analysis.

- Revenue tiers reflect real operational differences. The three tiers (under $1M, $1M to $3M, $3M+) are not arbitrary groupings. Cost structure, staffing models, overhead leverage, and growth patterns change meaningfully as companies move between them. Always benchmark yourself against your own tier first.

- The dataset spans seven U.S. regions. Mid-Atlantic, North Central, North East, Pacific Northwest, South Central, South East, and South West. The South East (35 operators) and South West (33) carry the largest samples. North Central (4 operators) should be interpreted as directional, not definitive.

- Geography is a secondary lens, not the primary one. Use your revenue tier to establish your primary comparison. Then layer in regional benchmarks where they are relevant to your market conditions, labor costs, or pricing environment.

- This data was not self-reported. Unlike survey-based industry studies, these numbers come from actual bookkeeping records standardized by FRAXN before any comparison was made. That distinction matters when you are using the data to make real decisions.

Find Your Peer Group

Knowing your revenue tier and region is the starting point for benchmarking. FRAXN builds the financial infrastructure that makes this kind of comparison possible for individual operators. Visit fraxn.com or scan the QR code to get started.

Revenue growth, or top-line growth, is the starting point for evaluating operating performance and overall financial results. This chapter examines how operators expanded revenue from 2023 through 2025, first through a multi-year stability lens (Cohort A, n = 60), and then through the 2024–2025 comparable benchmark cohort (Cohort B, n = 116) to provide a clearer view of recent performance.

The objective is twofold: to assess growth consistency over time and to evaluate how current growth performance is distributed across comparable peers. All statistics are presented as company-weighted distributions.

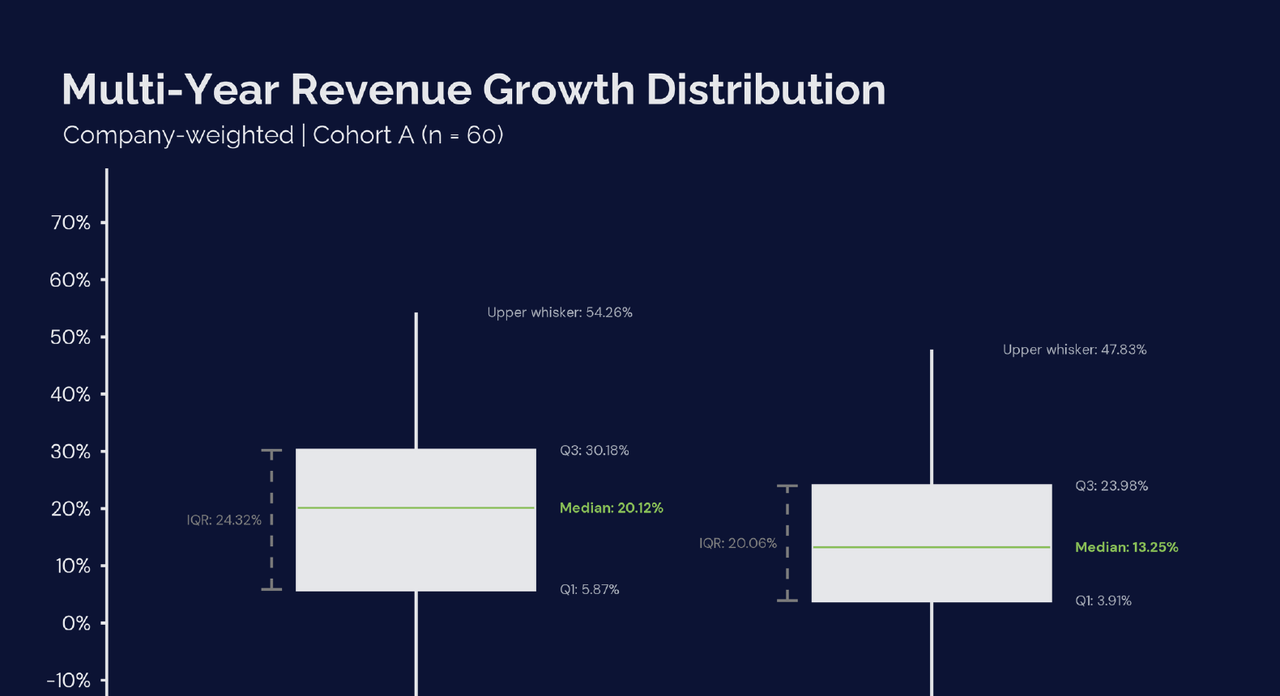

5.1 Multi-Year Growth Stability (2023–2025 | Cohort A n = 60)

To assess growth consistency and volatility, a subset of 60 operators with complete financial data from 2023 through 2025 was analyzed separately. Multi-year trend analysis uses this cohort only and should not be compared directly to the 125-company 2024–2025 benchmark dataset. Revenue tiers for multi-year analysis are fixed using 2024 baseline revenue to prevent tier shifting across years.

| Metrics | 2023→2024 | 2024→2025 | Description |

|---|---|---|---|

| Q1 (25th percentile) | 5.87% | 3.91% | Represents the lower quartile of Revenue Growth across operators for each period. |

| Median | 20.12% | 13.25% | Represents the typical Revenue Growth achieved by operators in each period. |

| Q3 (75th percentile) | 30.18% | 23.98% | Represents the upper quartile of Revenue Growth across operators for each period. |

| IQR (Q3–Q1) | 24.32 pp (percentage points) | 20.06 pp (percentage points) | Represents the spread between the 25th and 75th percentiles. |

This snapshot provides a benchmarking view of revenue growth stability across operators over the past two periods. While the interquartile range (Q3–Q1) indicates a relatively concentrated band of growth outcomes within the sample, the median growth rate declined from 20.12% in 2023–2024 to 13.25% in 2024–2025, a decrease of 6.87 percentage points (approximately 34%). This indicates that median revenue growth slowed materially between the two periods, reflecting a broad moderation in industry growth momentum rather than isolated underperformance.

The elevated growth environment in 2023–2024 also created conditions where operational inefficiencies could be masked or overlooked, as strong top-line expansion offset underlying cost pressures. As growth normalizes in 2024–2025, these inefficiencies become more visible, placing greater emphasis on cost structures and operating discipline.

As growth rates normalize, operators can no longer rely on top-line expansion alone to sustain profitability. Businesses built around aggressive growth capital deployment may begin to experience margin pressure as revenue expansion slows while cost structures remain elevated.

Operators should evaluate whether their current cost structure, staffing levels, and growth investments remain appropriate under a slower growth environment, and identify where operational efficiency or pricing adjustments may be required to maintain profitability.

| Category | 2023→2024 Companies (%/n) | 2024→2025 Companies (%/n) | Description |

|---|---|---|---|

| Hyper Growth (≥ 100%) | 5.00% (3) | 1.67% (1) | A small subset of operators experiencing exceptionally rapid revenue growth, typically associated with acquisitions or major scaling events. |

| Large Growth (≥ 30% and < 100%) | 20.00% (12) | 10.00% (6) | Operators delivering strong revenue expansion, often reflecting accelerated customer acquisition, new service lines, or market expansion. |

| Growing (≥ 0% and < 30%) | 58.33% (35) | 65.00% (39) | Represents majority of the operators achieving steady year-over-year revenue growth. |

| Declining (> -15% and < 0%) | 15.00% (9) | 15.00% (9) | Operators reporting moderate declines in revenue during the period. |

| Underperforming (≤ -15%) | 1.67% (1) | 8.33% (5) | Operators experienced significant revenue contraction year-over-year. |

The growth band distribution provides a benchmark view of how revenue expansion is distributed across operators over the two-year period.

Most companies have steady growth band (0–30%), indicating that moderate, consistent expansion represents the typical growth pattern in the industry.

However, the data also shows a noticeable shift between periods, with the share of operators experiencing significant contraction increasing from 1.67% in 2023–2024 to 8.33% in 2024–2025, while the proportion of companies achieving large or hyper growth declined.

These patterns signal that while growth remains common across the cohort, outcomes are becoming more uneven and moderating in recent years, reinforcing the need to benchmark performance and establish clear guardrails to peers, rather than relying solely on top-line growth.

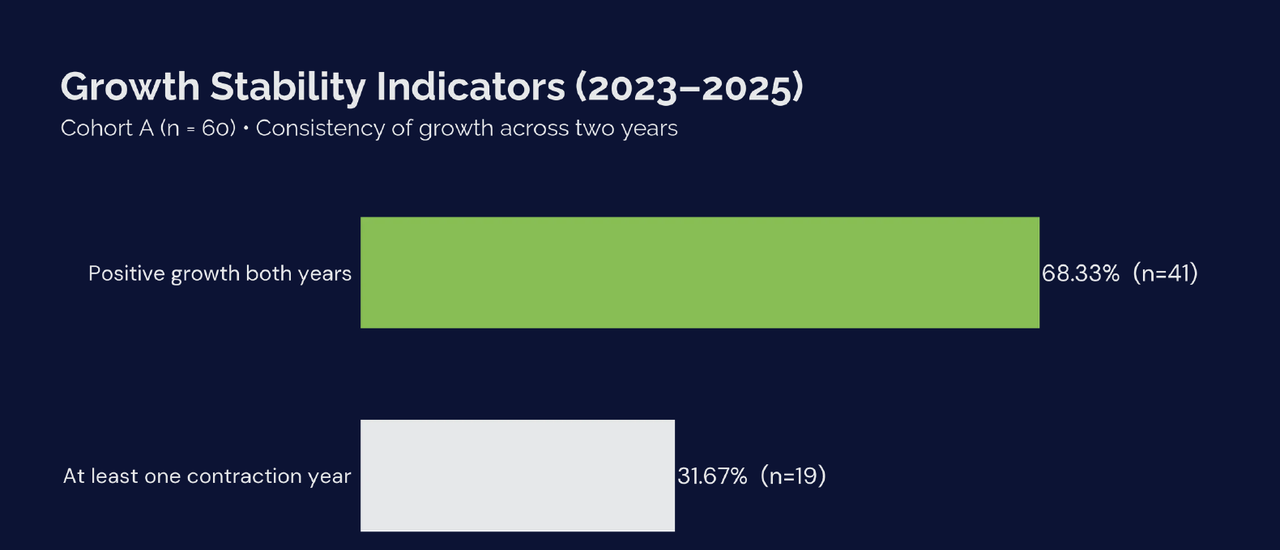

| Stability Metric | % of Companies | Operators (n) | Description |

|---|---|---|---|

| Positive growth both years | 68.33% | 41 | Operators that achieved revenue growth in both periods (2023–2024 and 2024–2025), indicating sustained expansion across the two-year window. |

| At least one contraction year | 31.67% | 19 | Operators that experienced a revenue decline in at least one of the two periods, reflecting some degree of growth volatility. |

| Declined both years | 8.33% | 5 | Operators that reported revenue contraction in both periods, indicating persistent negative growth over the two-year window. This is a subset of operators that experienced at least one contraction year. |

While industry expansion remains structurally intact, growth rates appear to be moderating. Approximately 68% of operators generated positive Revenue Growth in both periods, indicating sustained expansion across much of the sample. However, nearly one-third of companies experienced at least one contraction year. This pattern points out that growth stability is not universal across operators. Even within an expanding industry, individual operators may face volatility driven by local market conditions, customer churn, pricing pressure, or operational execution.

Operators should evaluate whether their growth model is resilient across multiple periods by examining customer retention, route density, and sales and marketing effectiveness to reduce the risk of intermittent revenue contraction.

5.2 Industry Growth Remains Positive but Performance is Fragmented

This section shifts from the multi-year cohort to the broader benchmark cohort to evaluate the most recent year-over-year performance from 2024 to 2025.

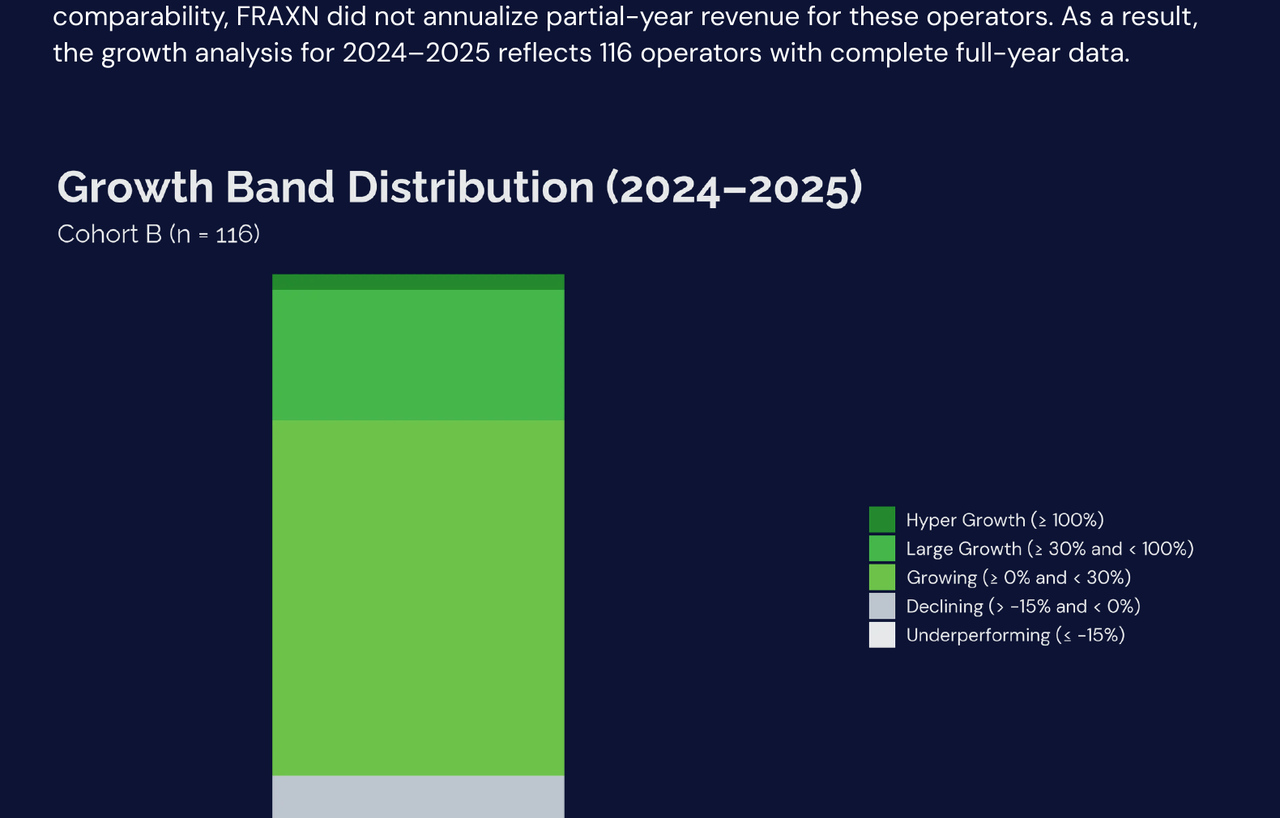

While the benchmark dataset includes 125 operators, nine companies began operations midway through 2024 and therefore do not reflect a full baseline year. To maintain comparability, FRAXN did not annualize partial-year revenue for these operators. As a result, the growth analysis for 2024–2025 reflects 116 operators with complete full-year data.

| Growth Band | % of Companies | Operators (n) | Description |

|---|---|---|---|

| Hyper Growth (≥ 100%) | 2.6% | 3 | A small subset of operators experiencing exceptionally rapid revenue growth, typically associated with acquisitions or major scaling events. |

| Large Growth (≥ 30% and < 100%) | 21.6% | 25 | Operators delivering strong revenue expansion, often reflecting accelerated customer acquisition, new service lines, or market expansion. |

| Growing (≥ 0% and < 30%) | 58.6% | 68 | Represents majority of the operators achieving steady year-over-year revenue growth. |

| Declining (> -15% and < 0%) | 12.1% | 14 | Operators reporting moderate revenue declines during the period. |

| Underperforming (≤ -15%) | 5.2% | 6 | Operators experiencing significant revenue contraction year-over-year. |

The findings across the benchmark group remain consistent. Revenue growth remained broadly positive, with approximately 83% of operators generating non-negative growth between 2024 and 2025 (Growing, Large Growth, and Hyper Growth), reinforcing the recurring revenue model that characterizes pest control services. The majority of operators (58.6%) fell within the moderate growth band of 0% to 30%, indicating that steady, incremental expansion remains the most common outcome across the industry.

However, performance outcomes are not uniform. While most operators grew, approximately 17.3% experienced some level of revenue contraction, including 5.2% with more pronounced declines. This variation highlights differences in execution, pricing power, service mix, and growth investment intensity across operators. Overall, the distribution suggests that growth is widespread but not evenly experienced, emphasizing that revenue expansion alone does not fully capture performance differences across the cohort.

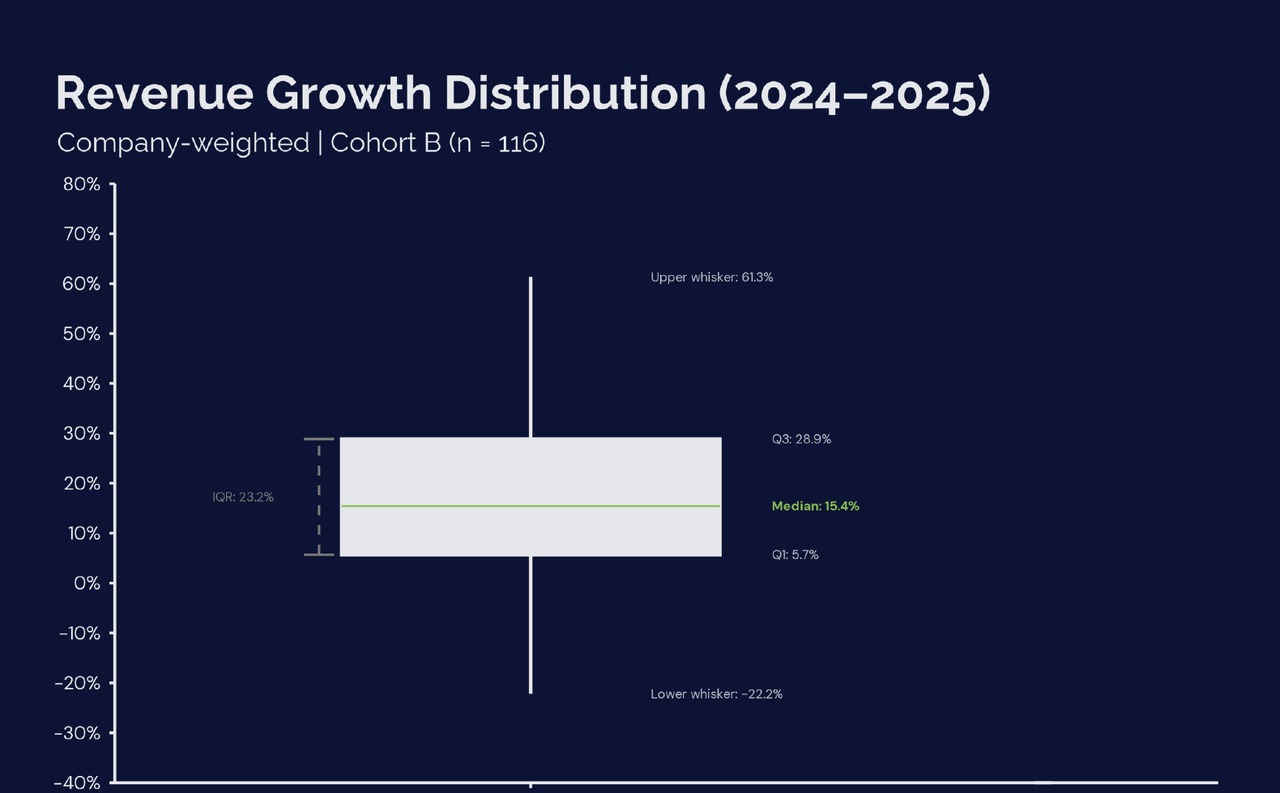

| Metric | Value |

|---|---|

| Q1 (25th percentile) | 5.7% |

| Median | 15.4% |

| Q3 (75th percentile) | 28.9% |

| IQR (Q3–Q1) | 23.2 pp |

Revenue expansion remains common across the industry, with the typical operator growing at 15.4% and most falling within a 5.7% to 28.9% range. This relatively wide middle band highlights that while growth is widespread, outcomes still vary meaningfully across operators. At the outer ends, a small number of companies experienced sharp contraction or outsized expansion, indicating that while extreme outcomes exist, they are not representative of the typical operator.

For this reason, growth should be viewed as a baseline rather than a signal of exceptional performance. Operators should assess performance relative to peers within their revenue tier, rather than relying on broad industry averages when identifying improvement opportunities.

5.3 Growth Diverges Materially by Revenue Tier

When segmented by revenue tier, growth outcomes diverge meaningfully across operators, indicating that scale influences both growth potential and volatility. Three structural distribution patterns emerge across the revenue tiers.

| Revenue Tier | Q1 (25th percentile) | Median | Q3 (75th percentile) | IQR (Q3–Q1) |

|---|---|---|---|---|

| <$1M | 12.7% | 20.6% | 39.5% | 26.8 pp |

| $1–3M | 3.4% | 9.9% | 27.5% | 24.1 pp |

| $3M+ | 2.9% | 15.8% | 24.4% | 21.5 pp |

<$1M — Rapid Expansion with Highest Variability

Smaller operators exhibit the fastest growth and the widest performance dispersion. Median growth reaches 20.6%, with upper-quartile outcomes approaching 40%, and the broadest interquartile range of 26.8 pp across tiers, highlighting the variability within this segment.

A meaningful portion of operators achieve very high growth rates, reflecting aggressive expansion from a smaller revenue baseline. At the same time, outcomes remain uneven as operators experiment with pricing strategies, marketing channels, and service mix.

This tier largely represents an expansion phase, where growth opportunities are abundant but operational structures are still developing.

$1–3M — The Structural Transition Zone

Growth moderates materially in the $1–3M segment. Median revenue growth declines to 9.9%, the slowest median outcome across all revenue tiers. While the typical operator performance in this segment continues to expand, the pace of growth becomes noticeably more constrained than in both smaller and larger peer groups. This pattern is consistent with the report's broader finding that the $1–3M range functions as a structural transition zone, where increasing organizational complexity begins to weigh on momentum.

At this stage, operators are often building the infrastructure required for the next phase of scale. Management layers begin to form, technician teams expand, and investment in sales and marketing becomes more formalized. These additions are necessary to support future growth, but they also introduce friction as costs and coordination requirements rise faster than the benefits of scale are fully realized.

In practical terms, the $1–3M tier represents an inflection point. Early-stage growth remains present, but it is no longer driven by lean, founder-led expansion alone. Operators that navigate this transition successfully are typically those that strengthen operating discipline while scaling, allowing systems, staffing, and revenue growth to mature in step rather than fall out of balance.

$3M+ — Stabilization and Operational Discipline

Larger operators demonstrate more stabilized growth outcomes, with median revenue growth rebounding to a modest 15.8% and dispersion narrowing relative to smaller peers. The interquartile range compresses to 21.5 percentage points, the lowest across all tiers, indicating more consistent performance across operators.

At this scale, operators benefit from more developed operational systems, greater route density, and more established pricing structures. These advantages support steadier performance, even as year-over-year comparisons become more demanding.

While explosive growth becomes less common, expansion in this tier increasingly reflects operational discipline and execution rather than rapid scaling from a smaller base.

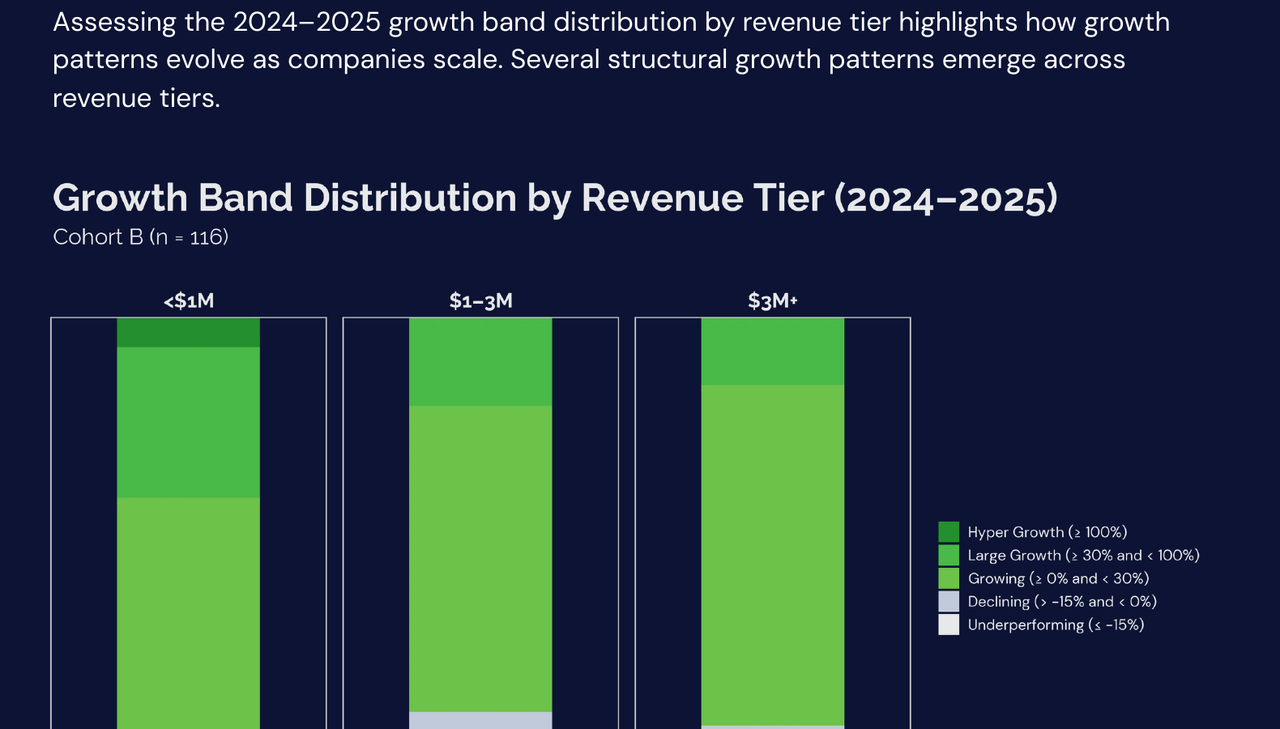

5.4 Growth Band Distribution by Tier

Assessing the 2024–2025 growth band distribution by revenue tier highlights how growth patterns evolve as companies scale. Several structural growth patterns emerge across revenue tiers.

| Growth Band | <$1M (n=52) | $1–3M (n=41) | $3M+ (n=23) |

|---|---|---|---|

| Hyper Growth (≥ 100%) | 5.8% (3) | — | — |

| Large Growth (≥ 30% and < 100%) | 28.8% (15) | 17.1% (7) | 13.0% (3) |

| Growing (≥ 0% and < 30%) | 55.8% (29) | 58.5% (24) | 65.2% (15) |

| Declining (> -15% and < 0%) | 1.9% (1) | 19.5% (8) | 21.7% (5) |

| Underperforming (≤ -15%) | 7.7% (4) | 4.9% (2) | — |

Note: Hyper-growth outcomes were not observed in the $1–3M and $3M+ tier during the study period. Also, no underperforming companies were observed on the $3M+ tier

Small operators dominate the high-growth tail

Among companies below $1M, more than one-third achieve growth above 30%, and hyper-growth outcomes appear only within this tier. The smaller revenue base allows for rapid percentage expansion as operators scale routes, technicians, and marketing investment.

Mid-sized operators experience the sharpest growth compression

In the $1–3M segment, hyper-growth disappears and the share of companies achieving large growth declines by roughly half compared with the <$1M tier. At the same time, nearly one-fifth of operators report declining revenue, indicating that increasing organizational complexity begins to offset early-stage expansion momentum.

Larger operators shift toward steadier but less explosive growth

Companies above $3M cluster heavily within the moderate growth band (0–30%). While some contraction occurs as markets mature and year-over-year comparisons become more demanding, growth outcomes tend to be more stable and less volatile than those observed among smaller peers.

Overall, patterns in both the revenue growth distribution and growth band across revenue tiers signal a common scaling trajectory: rapid early expansion, a mid-market compression phase, and eventual stabilization as operational systems mature.

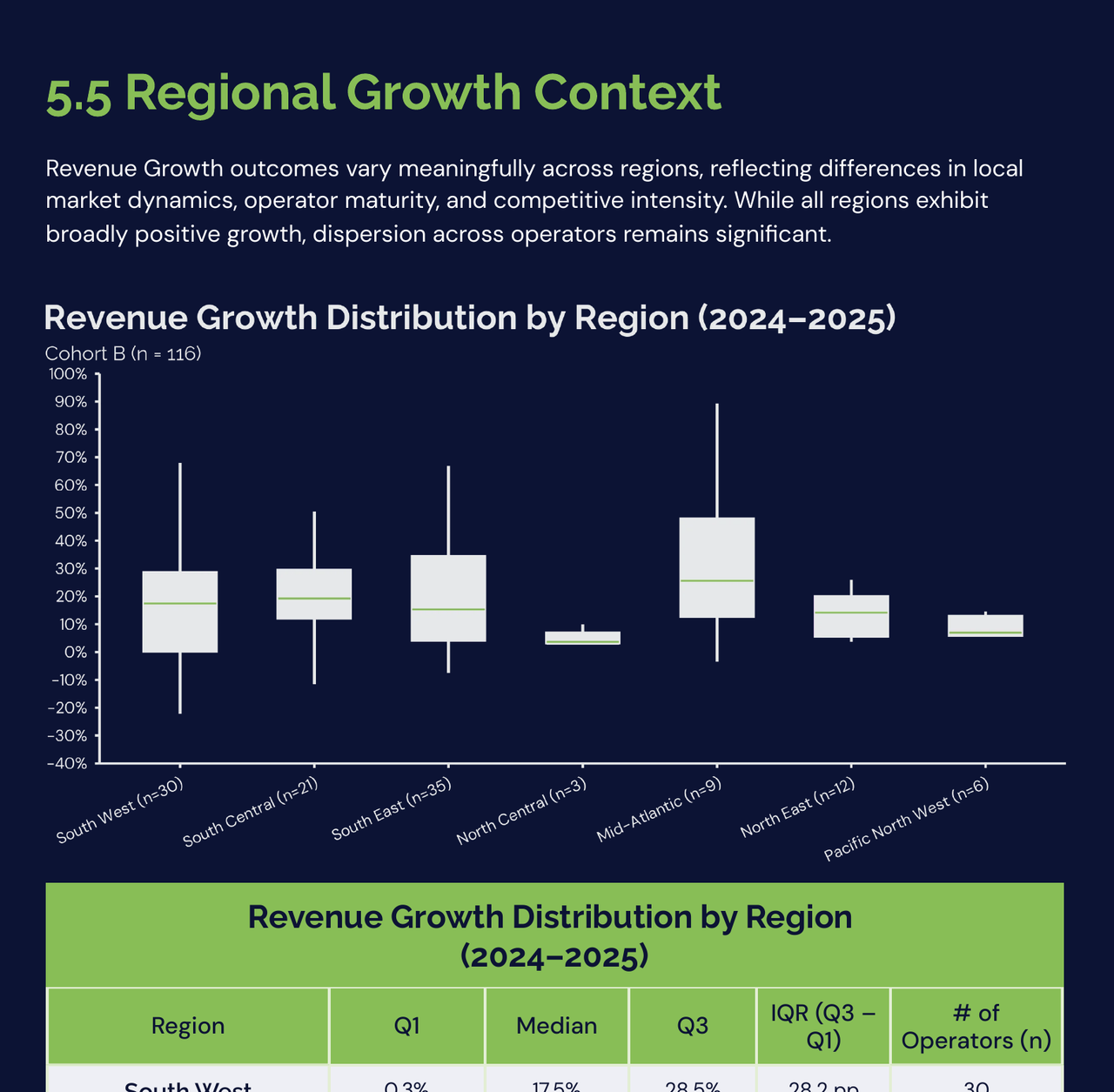

5.5 Regional Growth Context

Revenue Growth outcomes vary meaningfully across regions, reflecting differences in local market dynamics, operator maturity, and competitive intensity. While all regions exhibit broadly positive growth, dispersion across operators remains significant.

| Region | Q1 | Median | Q3 | IQR (Q3 – Q1) | # of Operators (n) |

|---|---|---|---|---|---|

| South West | 0.3% | 17.5% | 28.5% | 28.2 pp | 30 |

| South Central | 12.2% | 19.3% | 29.4% | 17.2 pp | 21 |

| South East | 4.2% | 15.3% | 34.3% | 30.1 pp | 35 |

| North Central | 3.3% | 3.7% | 6.8% | 3.5 pp | 3 |

| Mid-Atlantic | 12.8% | 25.6% | 47.8% | 35.0 pp | 9 |

| North East | 5.7% | 14.2% | 20% | 14.3 pp | 12 |

| Pacific North West | 6% | 7% | 12.9% | 6.90 pp | 6 |

Median growth ranges from 3.7% in North Central to 25.6% in the Mid-Atlantic, indicating that growth conditions vary across regional markets. However, variability within regions remains substantial, ranging from 3.5 pp to 35 pp, reinforcing that operator execution and local market positioning play a significant role in determining outcomes.

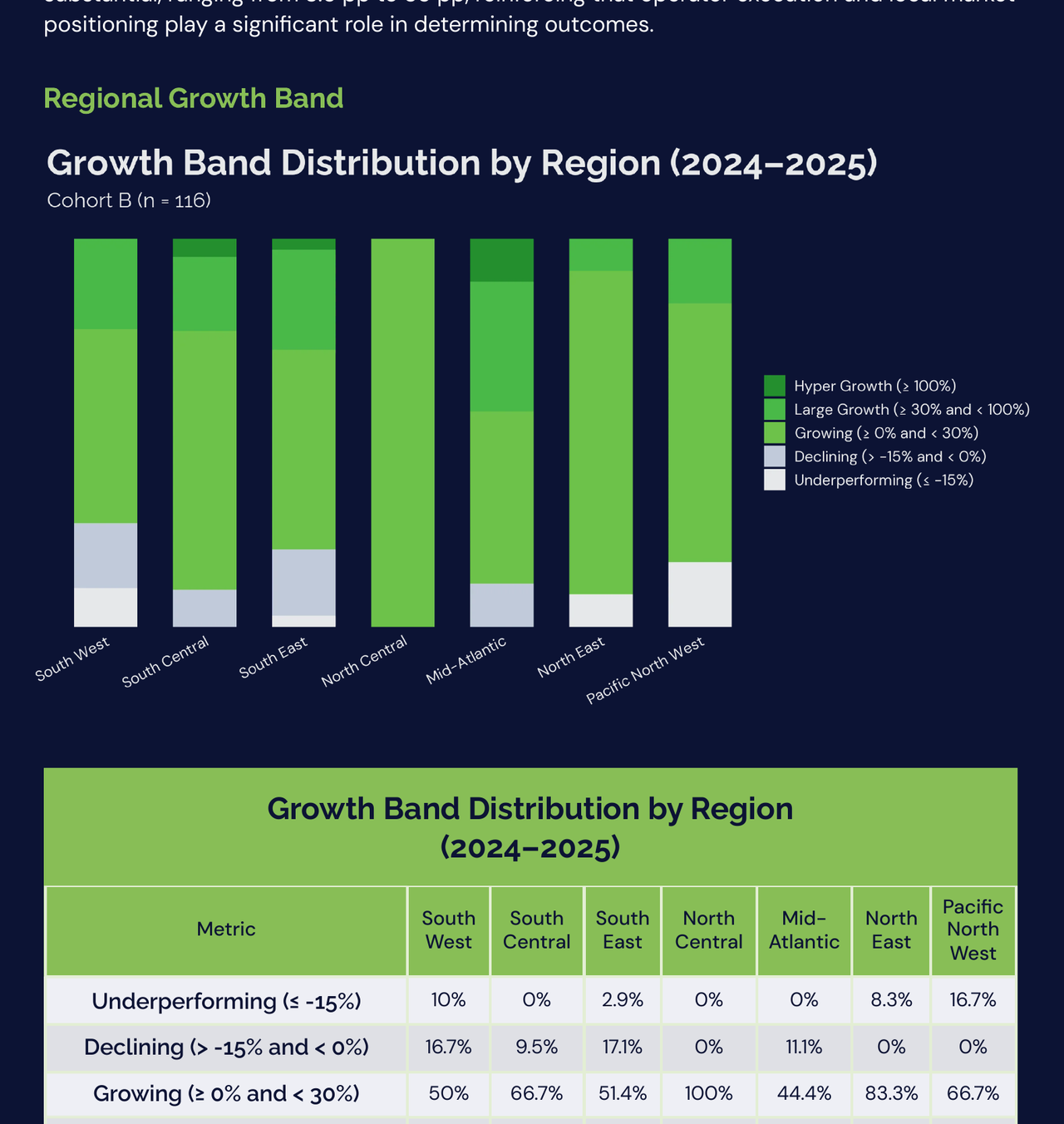

Regional Growth Band

| Metric | South West | South Central | South East | North Central | Mid-Atlantic | North East | Pacific North West |

|---|---|---|---|---|---|---|---|

| Underperforming (≤ -15%) | 10% | 0% | 2.9% | 0% | 0% | 8.3% | 16.7% |

| Declining (> -15% and < 0%) | 16.7% | 9.5% | 17.1% | 0% | 11.1% | 0% | 0% |

| Growing (≥ 0% and < 30%) | 50% | 66.7% | 51.4% | 100% | 44.4% | 83.3% | 66.7% |

| Large Growth (≥ 30% and < 100%) | 23.3% | 19% | 25.7% | 0% | 33.3% | 8.3% | 16.7% |

| Hyper Growth (≥ 100%) | 0% | 4.8% | 2.9% | 0% | 11.1% | 0% | 0% |

Across most regions, the Growing or Moderate Growth Band (0–30%) captures most operators, indicating steady expansion across the industry, regardless of Region. However, the presence of both high-growth and declining operators in several regions highlights meaningful performance dispersion.

Regional Observations

Mid-Atlantic | Strongest Growth Momentum

The Mid-Atlantic region exhibits the strongest growth profile in the dataset, with median growth reaching 25.6% and the upper quartile approaching 47.8%. Over 44% of operators achieved growth above 30%, including 11.1% reaching hyper-growth levels. Notably, no operators in this region reported severe contraction.

South Central and South East | Balanced Expansion

South Central and South East demonstrate balanced growth distributions. Median growth reaches 19.3% and 15.3%, respectively, with strong representation in the moderate growth band. Large-growth outcomes are also common, with roughly 19–26% of operators exceeding 30% growth.

South West | Higher Dispersion

The South West shows greater variability in outcomes. While median growth remains solid at 17.5%, roughly 27% of operators experienced negative growth, alongside a meaningful share achieving strong expansion. This indicates a more polarized performance environment.

North East | Moderate but Stable

The North East demonstrates moderate but relatively stable growth, with median growth at 14.2% and most operators clustered in the moderate growth band.

Pacific North West | Slower Expansion

The Pacific North West shows slower growth dynamics, with median growth of 7.0%. Most operators fall within the moderate growth range, indicating steady but more measured expansion.

North Central | Limited Sample

The North Central region reports the lowest median growth at 3.7%, though the sample size is limited (n = 3). Results should therefore be interpreted cautiously.

Regional Data Considerations

Regional analysis is based on 116 operators with complete 2024–2025 revenue data. Participation varies significantly by region, with larger samples in the South East (n = 35) and South West (n = 30) providing more reliable signals.

Smaller samples particularly North Central (n = 3) and Pacific North West (n = 6) should be interpreted as directional rather than definitive.

Broadly, the regional analysis suggests that growth dispersion across operators is often greater than differences between regions themselves, indicating that operator execution, pricing strategy, and service mix likely play a larger role in growth outcomes than geography alone.

5.6 Chapter Summary: Growth is Non-Linear with Scale

Growth across pest control operators does not progress linearly with revenue size. Instead, the data suggests a three-stage scaling pattern:

- Small operators grow rapidly but with high variability.

- Mid-sized operators encounter structural friction as organizational complexity increases.

- Larger operators stabilize as operational systems, pricing discipline, and route density mature.

Scaling from <$1M to $3M+ therefore requires more than market demand. It typically requires operating redesign, including stronger technician management systems, clearer pricing discipline, route optimization, and more formalized sales infrastructure.

Operators that fail to adapt their operating structure during this transition often experience a prolonged mid-tier plateau, where growth slows despite continued market opportunity. The data indicates this inflection point is driven less by demand conditions and more by internal operational complexity.

Across both regional and revenue-tier views, the data shows that while geographic market conditions influence growth potential, structural factors, particularly scale, operating systems, and growth strategy, may play a more important role in shaping long-term performance outcomes.

tldr; Chapter 5 — Revenue Performance Trends (2023–2025)

Summary Points

- The industry is still growing, but growth is normalizing. Median Revenue Growth was 15.4% between 2024 and 2025. That is healthy. But the share of operators experiencing meaningful contraction increased from 1.7% in the prior period to 8.3%. Growth is still the norm, but it is becoming less uniform.

- 84% of operators grew. Non-negative growth was the rule, not the exception. But 17.3% of operators experienced some level of revenue decline, a reminder that this industry is not immune to execution risk, pricing pressure, or competitive intensity.

- Growth follows a three-stage pattern by revenue tier. Under $1M operators grow fastest but with the most variability (median 20.6%). The $1M to $3M range is the transition zone, where growth slows sharply to 9.9% as organizational complexity rises. Operators above $3M stabilize at 15.8% with tighter dispersion.

- The $1M to $3M tier is the hardest stage. This is not a performance problem. It is a structural one. Companies at this scale are building the management, staffing, and sales infrastructure required for the next phase. Growth often slows not because demand dried up, but because the operating model is being rebuilt.

- Regional differences are real but not deterministic. Median growth ranged from 3.7% in North Central to 25.6% in Mid-Atlantic. But within every region, the variation between operators was wider than the variation between regions. Where you operate matters less than how you operate.

- Growth consistency matters as much as growth rate. About 68% of operators in the three-year cohort showed positive revenue growth in both periods. Nearly one-third did not. Reliable recurring revenue through customer retention and route density is a stronger foundation than peak-year expansion.

Revenue Growth across the pest control industry has remained positive, though signs of moderation have emerged between 2024 and 2025. When growth begins to normalize, the relationship between expansion and profitability is increasingly determined by how effectively operators manage rising costs alongside revenue gains.

This chapter examines expense behavior across participating operators, focusing on multi-year cost structure trends, growth efficiency, and the cost drivers most closely linked to Margin performance.

Unless otherwise noted, analyses are based on Cohort B (n = 116) operators with full-year comparability between 2024 and 2025. Multi-year trend analysis references Cohort A (n = 60) operators with complete financial data from 2023–2025.

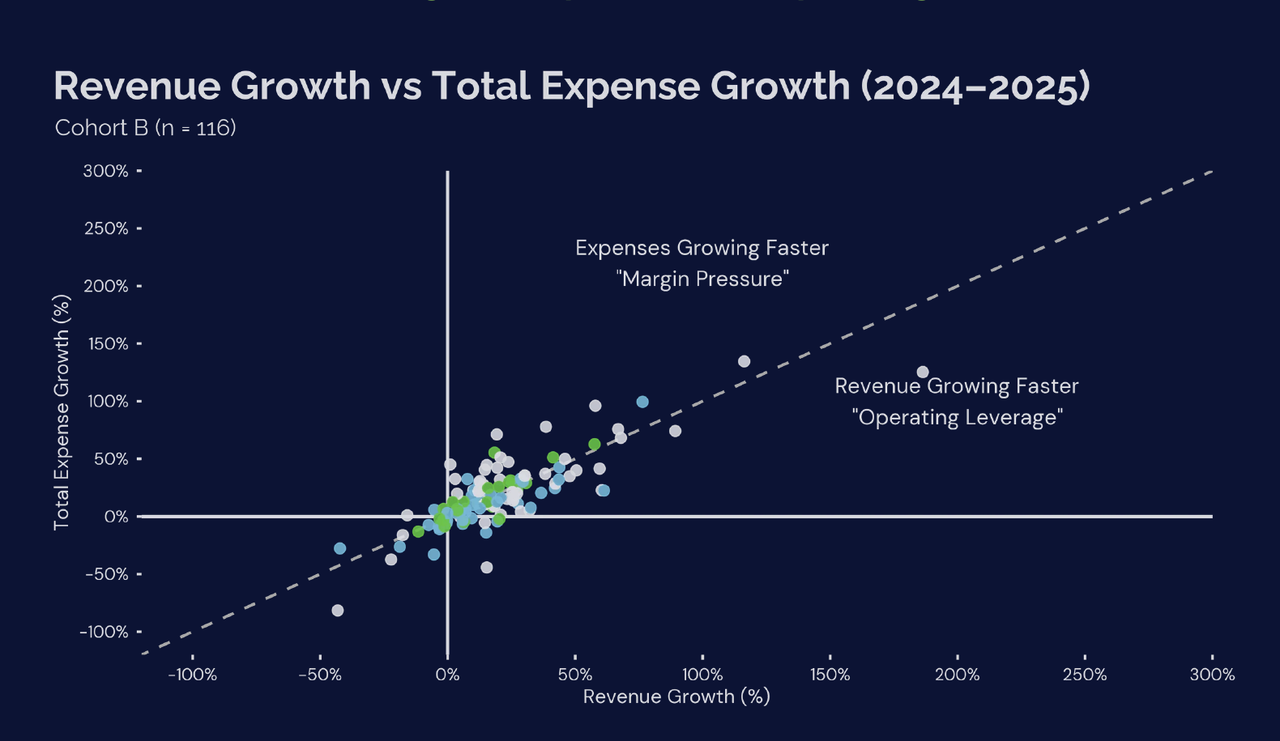

6.1 Revenue Growth vs Expense Growth (2024–2025)

| Quartile | Expense Growth | Revenue Growth |

|---|---|---|

| Q1 (25th percentile) | 3.1% | 5.7% |

| Median | 18.5% | 15.4% |

| Q3 (75th percentile) | 32.5% | 28.9% |

| IQR (Q3–Q1) | 29.4 pp | 23.2 pp |

Common misread: Higher median values are not always better. For Expense Growth, lower values indicate greater efficiency, as slower cost expansion reflects stronger cost control.

While top-line growth appears healthy, with median revenue increasing by 15.4% from 2024 to 2025 and an interquartile range of 23.2 percentage points, the cost side of the equation presents a more nuanced and often overlooked story. Growth naturally brings higher costs, but not all cost expansion scales evenly with revenue. Beneath the surface, overall Expense Growth was both more dispersed and structurally higher, with the middle 50% of companies seeing expenses increase between 3.1% (Q1) and 32.5% (Q3), representing a wider spread of 29.4 percentage points. This indicates that cost expansion outpaced Revenue Growth for a meaningful portion of operators. At the same time, the spread of results suggests that efficient scaling remains achievable as some operators were able to control cost expansion despite similar growth conditions.

The gap between revenue and Expense Growth provides evidence that a meaningful portion of operators are scaling without maintaining cost alignment. This pattern shows that while revenue is increasing, many operators are spending more to get there, with costs growing faster than the business itself.

Operators should shift focus from growth alone to how costs are scaling alongside revenue. Start by identifying the largest areas of cost expansion and assessing whether these increases are intentional and aligned with business needs. If expenses are growing faster than revenue, resist adding new costs and focus on correcting the drivers of increase such as improving technician utilization before hiring, validating marketing efficiency before scaling spend, and tightening overhead as the business scales. The goal is not to slow down growth, but to ensure that cost expansion remains controlled and aligned as the business scales.

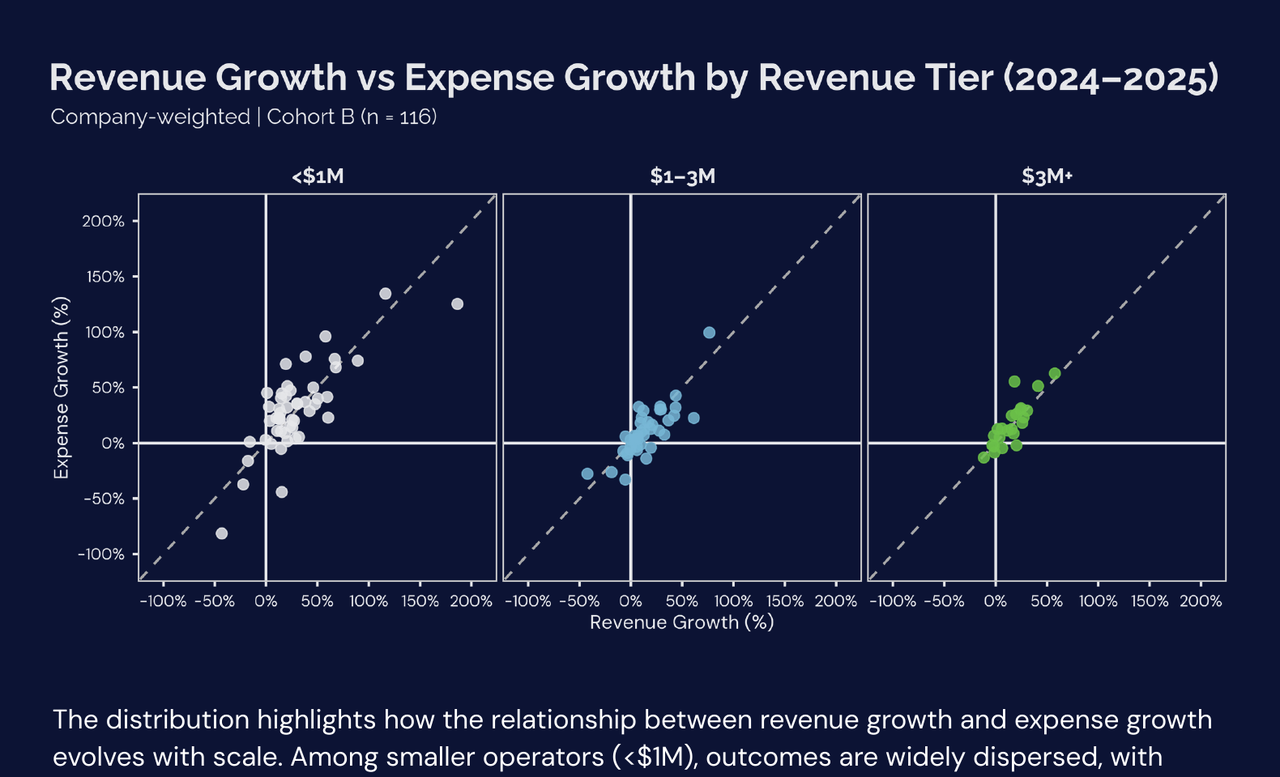

Plotting Revenue Growth against total Expense Growth quickly shows that a significant number of operators cluster close to the diagonal line, where costs rise with the same rate as revenue. However, equivalence between Revenue Growth and Expense Growth is not sufficient to create efficient gains or better Margins. Of the 116 operators analyzed, 56 experienced Expense Growth outpacing revenue, while 60 achieved Revenue Growth ahead of expenses, representing a near-even split between less efficient and more efficient growth outcomes.

Operators above the diagonal line, where Expense Growth exceeds Revenue Growth, are expanding their cost base faster than their top line, indicating rising cost intensity and Margin pressure.

Conversely, operators below the diagonal line demonstrate stronger operating leverage, with Revenue Growth outpacing expense expansion. These businesses were able to scale with relatively less incremental cost, creating operating leverage.

At a cohort level, this distribution highlights a key structural divide: growth efficiency varies widely across operators. Companies with similar Revenue Growth trajectories can operate very differently depending on how effectively costs scale alongside that growth.

The distribution highlights how the relationship between revenue growth and expense growth evolves with scale. Among smaller operators (<$1M), outcomes are widely dispersed, with points spread across both sides of the diagonal. This indicates inconsistent cost control, where some operators successfully translate growth into operating leverage, while others experience expense growth that outpaces revenue, creating margin pressure. This variability reflects the challenges of scaling labor, absorbing overhead, and managing growth investment on a smaller scale.

As operators grow, this dispersion narrows. In the $1–3M tier, results begin to cluster more closely around the diagonal, suggesting improved alignment between revenue expansion and cost growth. By the time operators reach $3M+, the distribution tightens further, with most companies operating within a narrower range. This reflects greater cost discipline, more predictable scaling of labor, and stronger operating control as businesses mature.

Across all tiers, a consistent pattern emerges: many operators cluster near the diagonal, where revenue and expenses grow at similar rates. This indicates that growth alone does not inherently translate into margin expansion. Instead, the ability to maintain separation below the diagonal, where revenue growth exceeds expense growth, is what distinguishes more efficient operators.

The key takeaway is not whether operators achieved growth, but how efficiently that growth was delivered. Discipline on Cost-of-Service Expenses and Operating Expenses remain the primary determinant of whether revenue expansion translates into improved profitability.

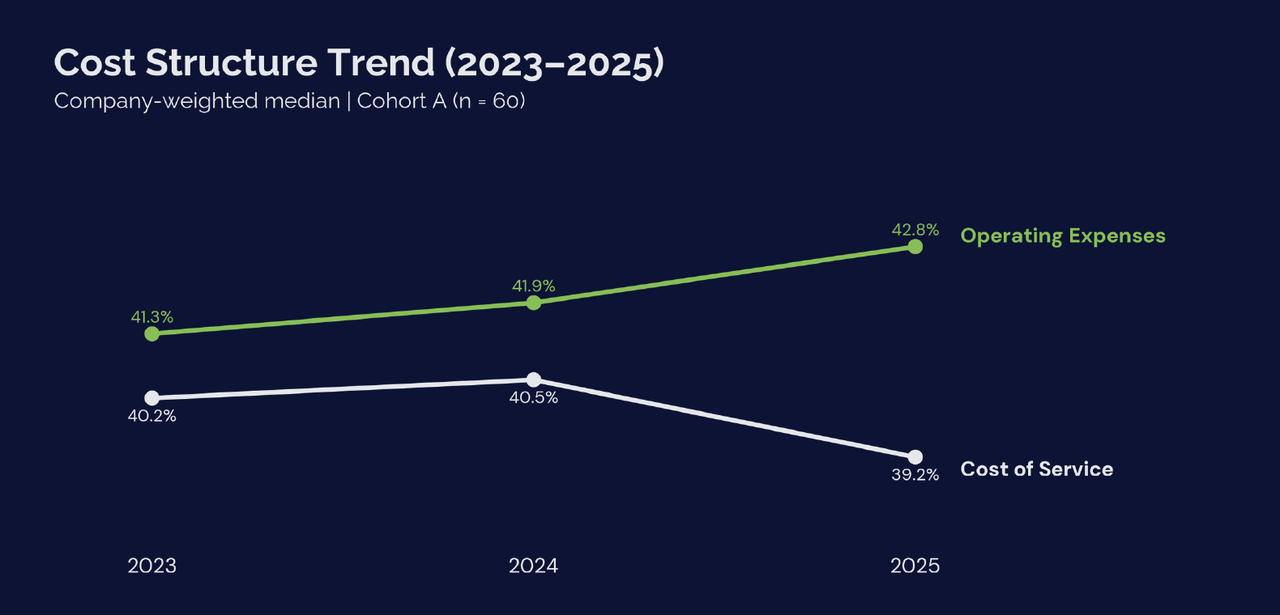

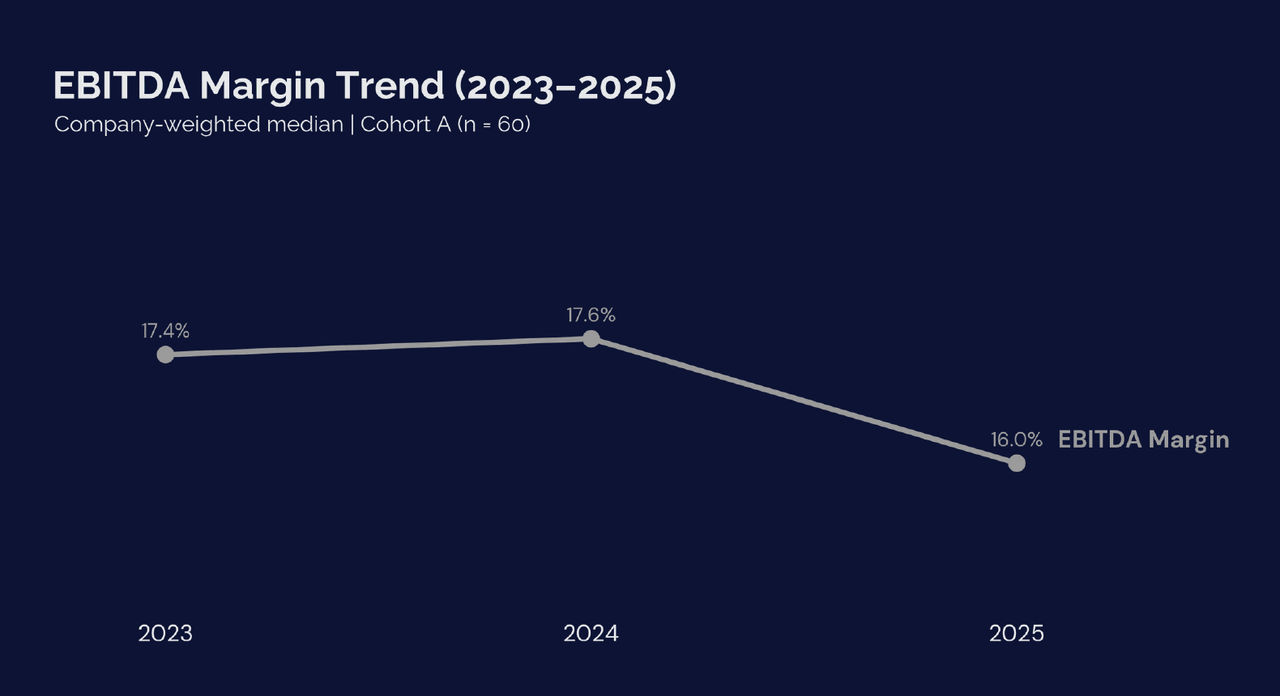

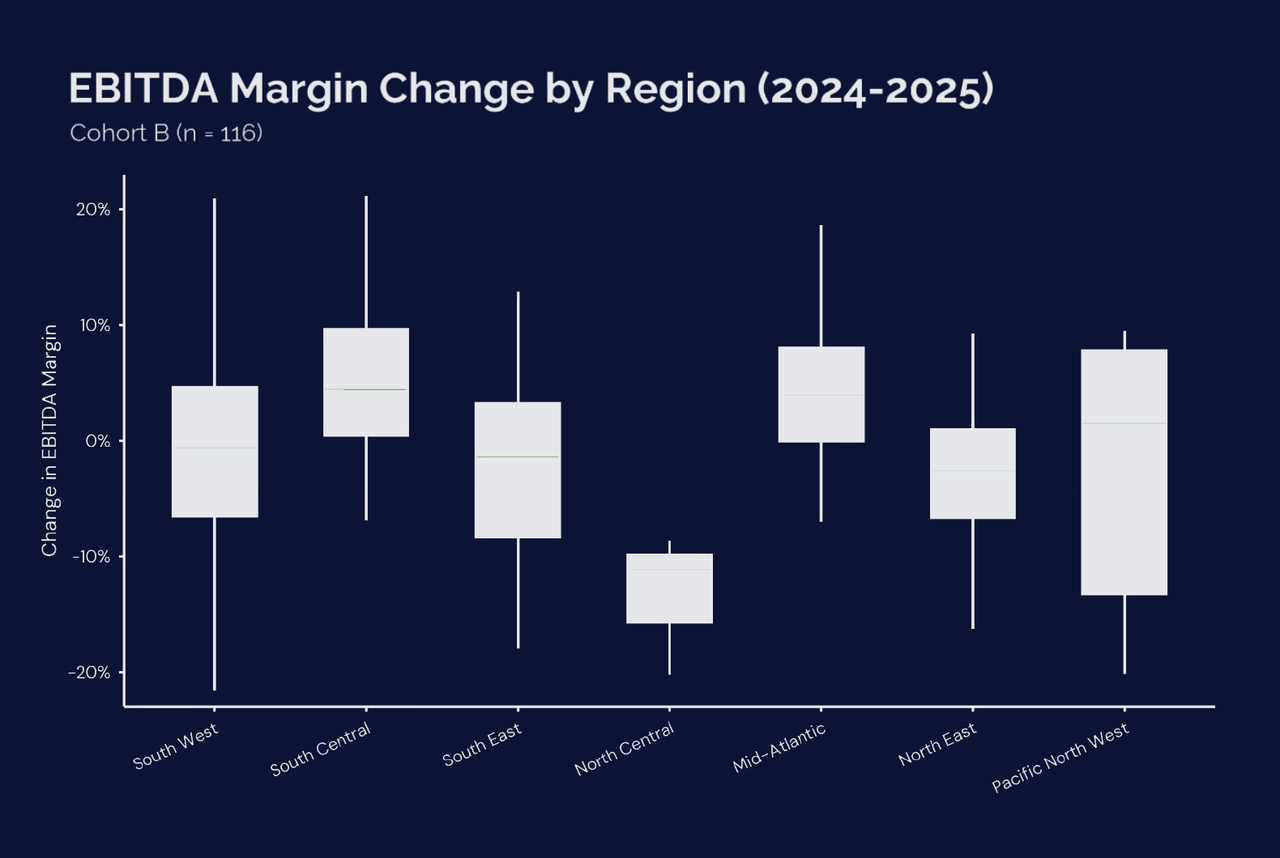

6.2 Multi-Year Cost Structure Trend (2023–2025)

Multi-year trend analysis shows that the industry cost structure has remained broadly stable, although modest shifts across key expense categories have gradually influenced performance.

Across the 2023–2025 period, Cost of Service remains a significant component of the cost structure for pest control operators, though Operating Expenses represent a larger share at the median.

Cost of Service includes technician labor, service vehicles, materials, small equipment and chemicals, and other direct field costs associated with delivering service. Median COS increased from 40.2% in 2023 to 40.5% in 2024, before declining to 39.2% in 2025, indicating modest improvements in field-level cost efficiency in the most recent period.

On the other hand, Median Operating Expenses, which include indirect labor, sales and marketing, facility costs, and administrative overhead, increased from 41.3% in 2023 to 41.9% in 2024 and further to 42.8% in 2025. This trend indicates sustained upward pressure on overhead and support functions as companies scale, with that pressure becoming more pronounced in the most recent year.

| Metric | 2023 Median | 2024 Median | 2025 Median |

|---|---|---|---|

| Cost of Service % | 40.2% | 40.5% ▲ | 39.2% ▼ |

| Operating Expenses % | 41.3% | 41.9% ▲ | 42.8% ▲ |

| EBITDA Margin % | 17.4% | 17.6% ▲ | 16.0% ▼ |

The time-series trend highlights an important shift in cost behavior across periods. From 2023 to 2024, median Cost of Service, OPEX, and EBITDA Margins all increased simultaneously, indicating that early-stage growth was supported by expanding cost structures without immediately eroding Margins. This can make underlying cost pressures less visible, allowing it to build as companies scale.

The pattern shifts from 2024 to 2025. Beneath the surface, continued cost expansion begins to outpace the moderating rate of revenue growth. As growth slows, the impact of rising costs becomes more visible, placing pressure on EBITDA margins, which show signs of compression in the most recent period.

These movements illustrate how shifts across cost layers interact. Even though direct service costs improved in 2025, this was more than offset by continued increases in Operating Expenses and slowing down of top-line growth, contributing to the compression of median EBITDA Margin from 17.6% in 2024 to 16.0% in 2025.

The data points to a clear signal: while operators have made progress managing direct service costs, rising overhead has become a more prominent driver of the overall cost structure. As businesses scale, maintaining discipline in operating expenses will be critical to sustaining performance.

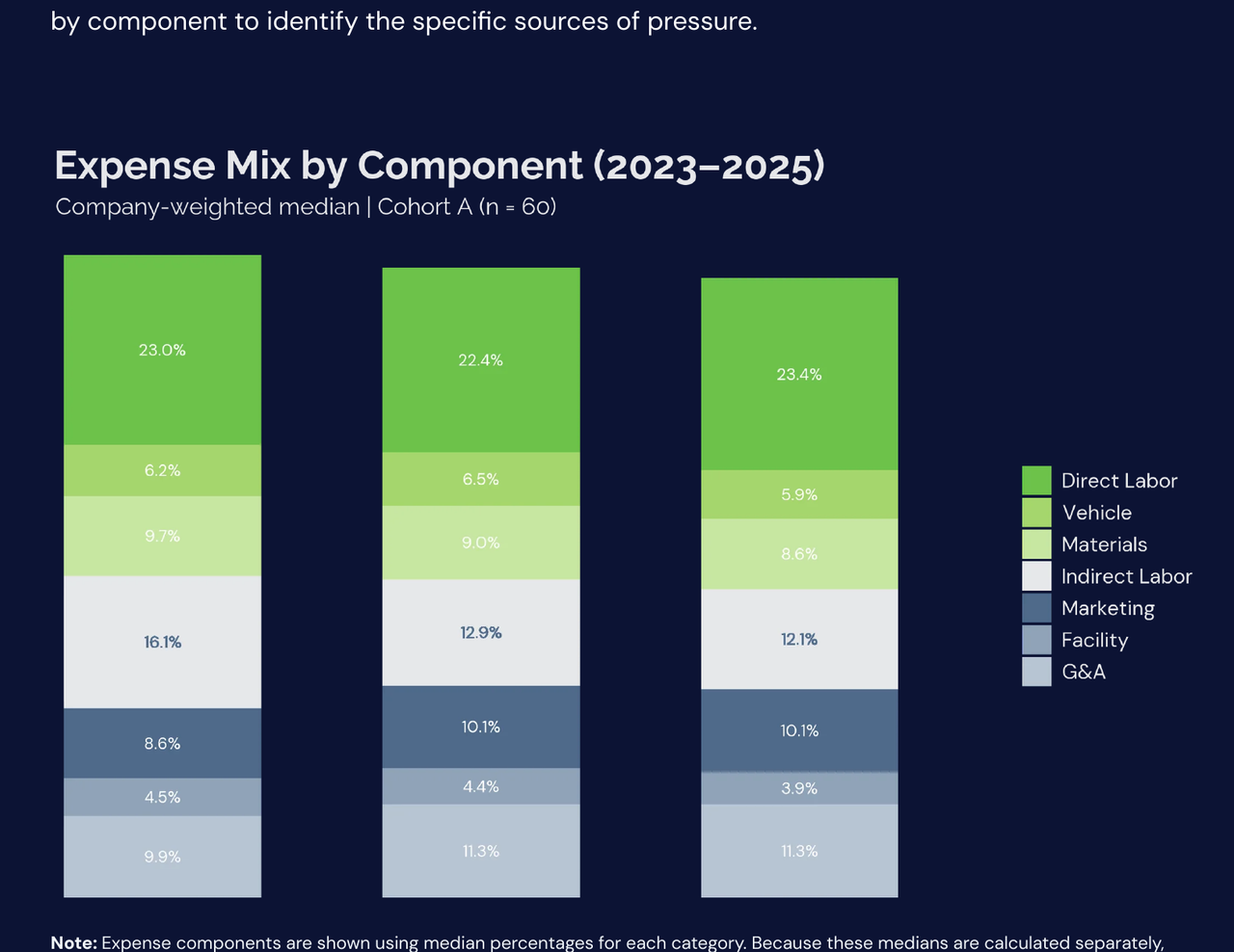

The cost structure trend indicates that recent changes are increasingly driven by operating expenses rather than direct service costs. The analysis therefore focuses on the expense mix by component to identify the specific sources of pressure.

Note: Expense components are shown using median percentages for each category. Because these medians are calculated separately, the stacked totals are intended to show the relative mix of costs rather than to exactly add up to the overall COS, OPEX, or EBITDA Margin.

Breaking down expenses by component shows that the industry cost structure remains heavily concentrated in labor-related categories. Direct service labor continues to represent the largest single expense category across operators, highlighting the importance of continued efficiency which was seen earlier.

Marketing, facilities, and general and administrative costs account for smaller portions of the expense base but form the core overhead supporting operations and growth. Across the three-year period, the relative composition of these components remained broadly stable.

This consistency on the expense mix for the 3 periods indicates that much of the industry's cost structure is structural rather than cyclical. Personnel costs, both direct and indirect, remain the largest component of total expenses, meaning that even modest changes in labor productivity or staffing structure can have a meaningful impact on overall cost levels.

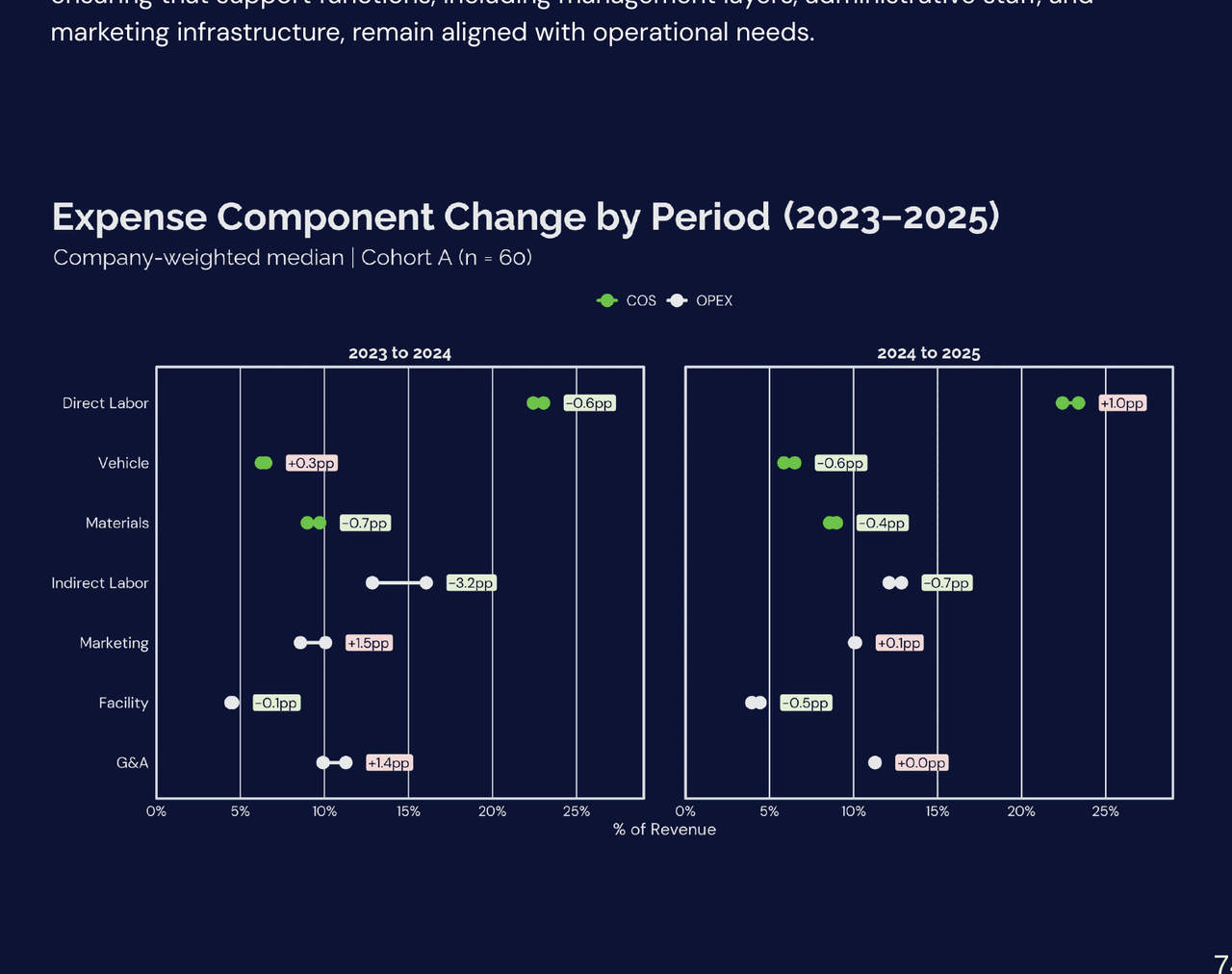

As a result, the focus shifts from broad cost reduction to disciplined cost scaling. Labor and overhead must grow in step with the business, maintaining technician productivity while ensuring that support functions, including management layers, administrative staff, and marketing infrastructure, remain aligned with operational needs.

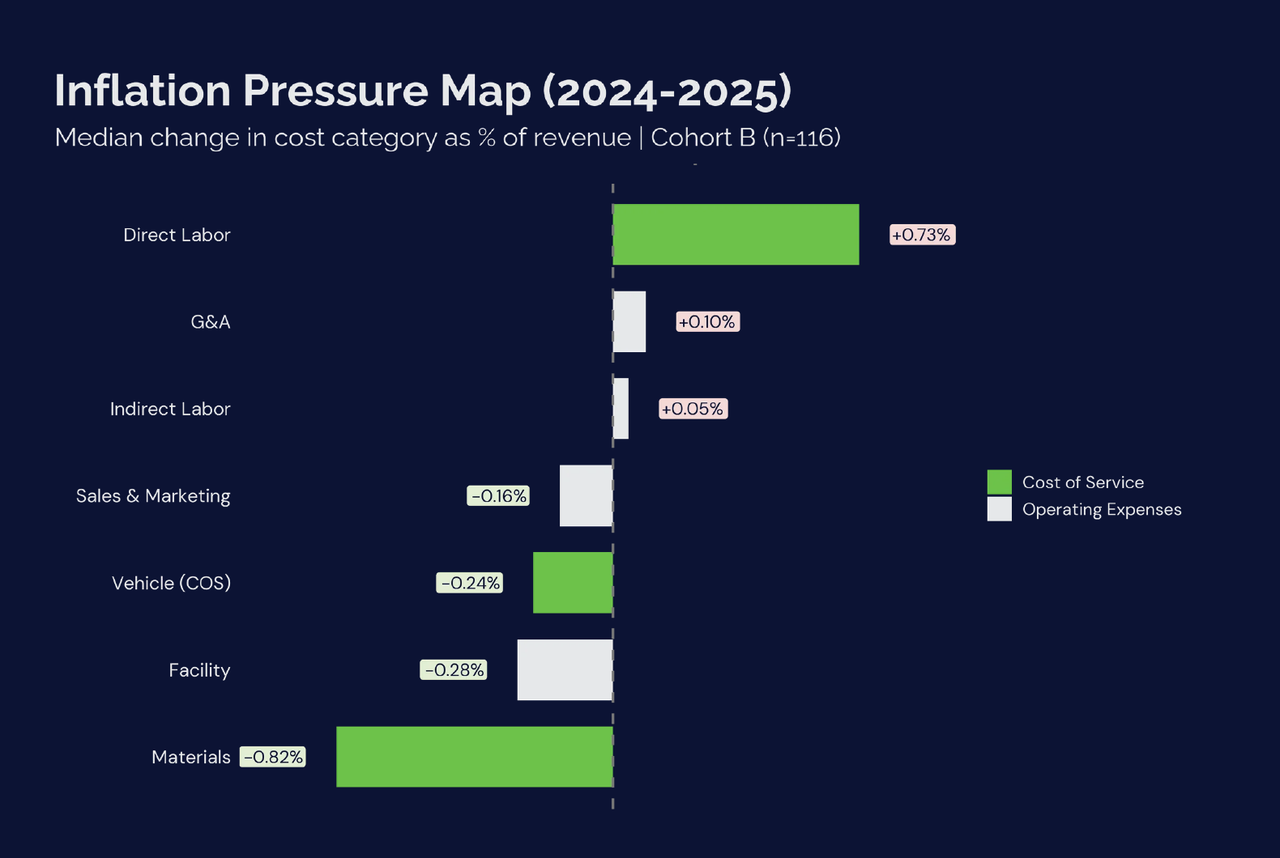

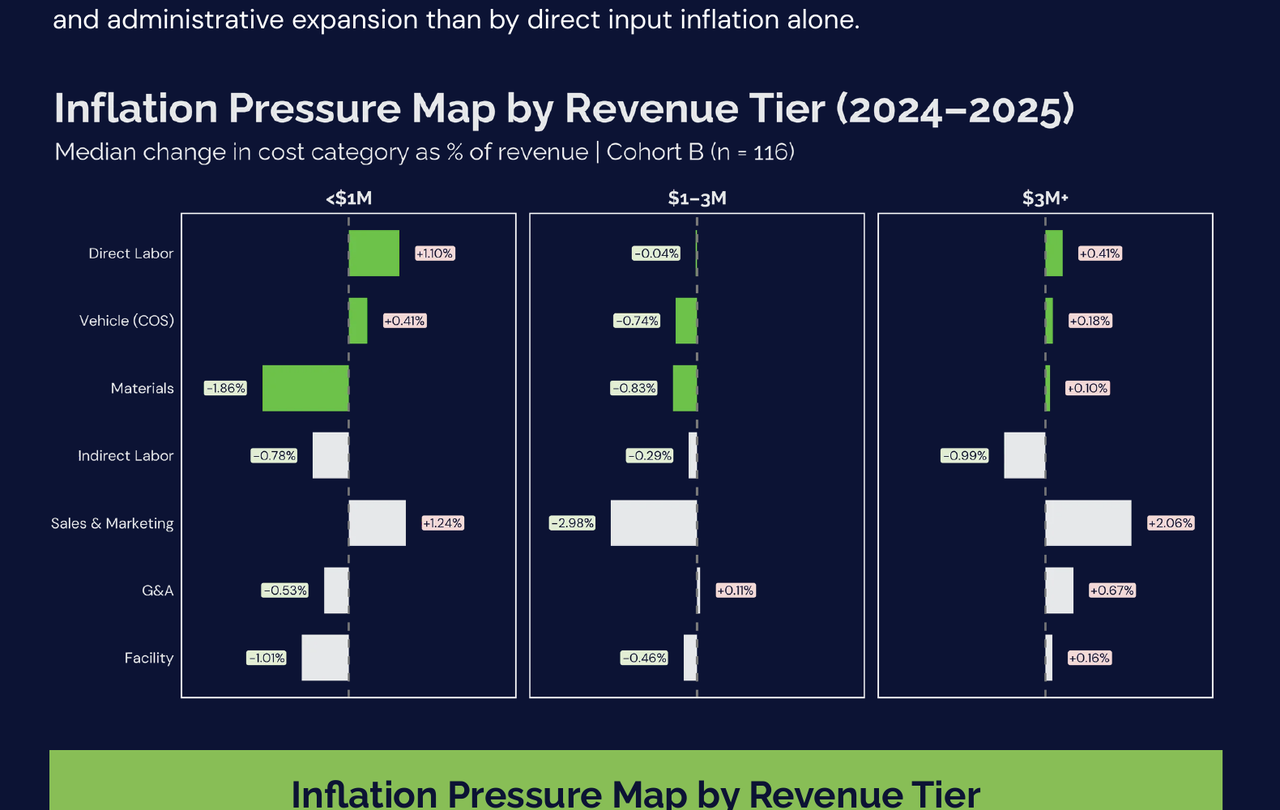

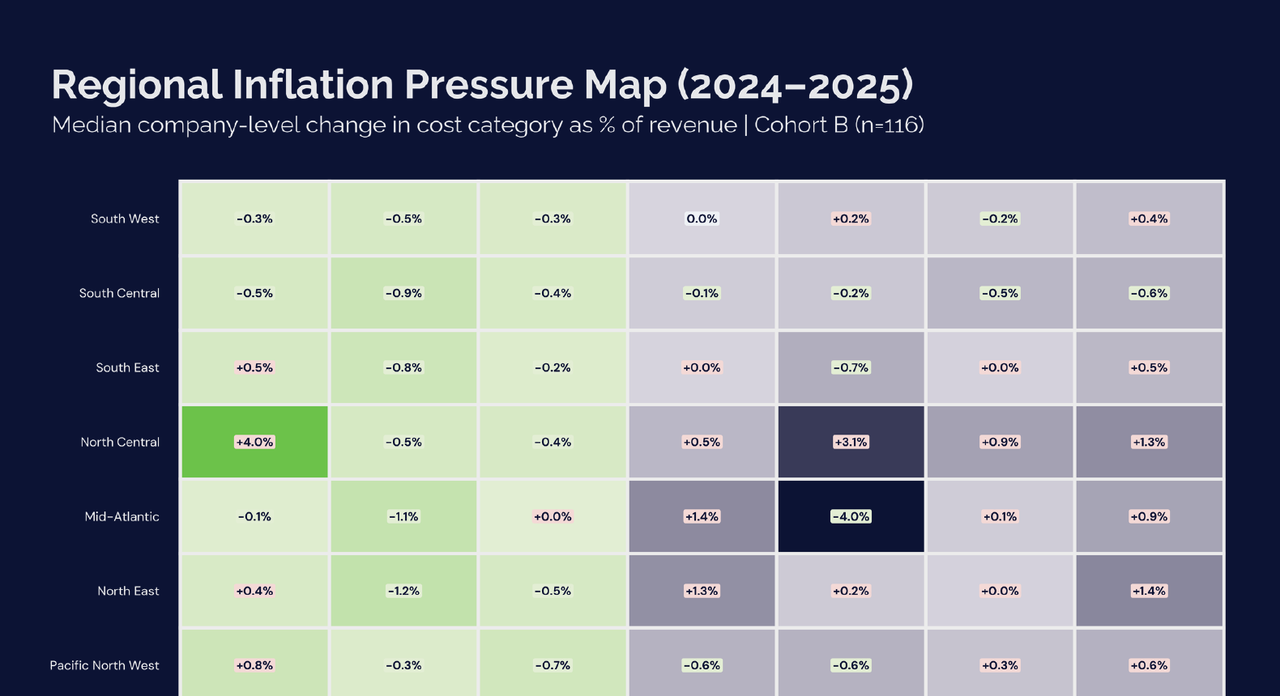

Year-over-year changes highlight where cost pressures have emerged. Between 2023–2024 and 2024–2025, several direct service cost categories stabilized or declined modestly. The main exception was direct labor, which increased by approximately one percentage point from 2024 to 2025.

In contrast, overhead categories, particularly marketing and G&A costs, showed more consistent upward movement across operators. Indirect labor, however, demonstrated the most noticeable improvement over the 2023–2025 period, suggesting that some operators have begun moderating the growth of support functions.

These observations shows that recent cost pressure reflects a combination of rising field labor costs and continued increase on growth investment as businesses scale. While several direct service costs stabilized or declined, increases in technician labor and ongoing investment in support functions continue to shape the overall cost structure.

Maintaining balance in cost structure will require operators to manage both sides of the equation, improving field productivity while ensuring that overhead growth remains aligned with operational needs.

Common Misreads:

- A stable expense mix does not mean costs are flat, absolute dollar value costs may still increase as the business grows.

- Lower COS does not necessarily indicate improved cost position if overhead expenses expand at the same time.

- Cost management is not about "cutting everything," but about identifying and addressing the largest and most impactful cost drivers.

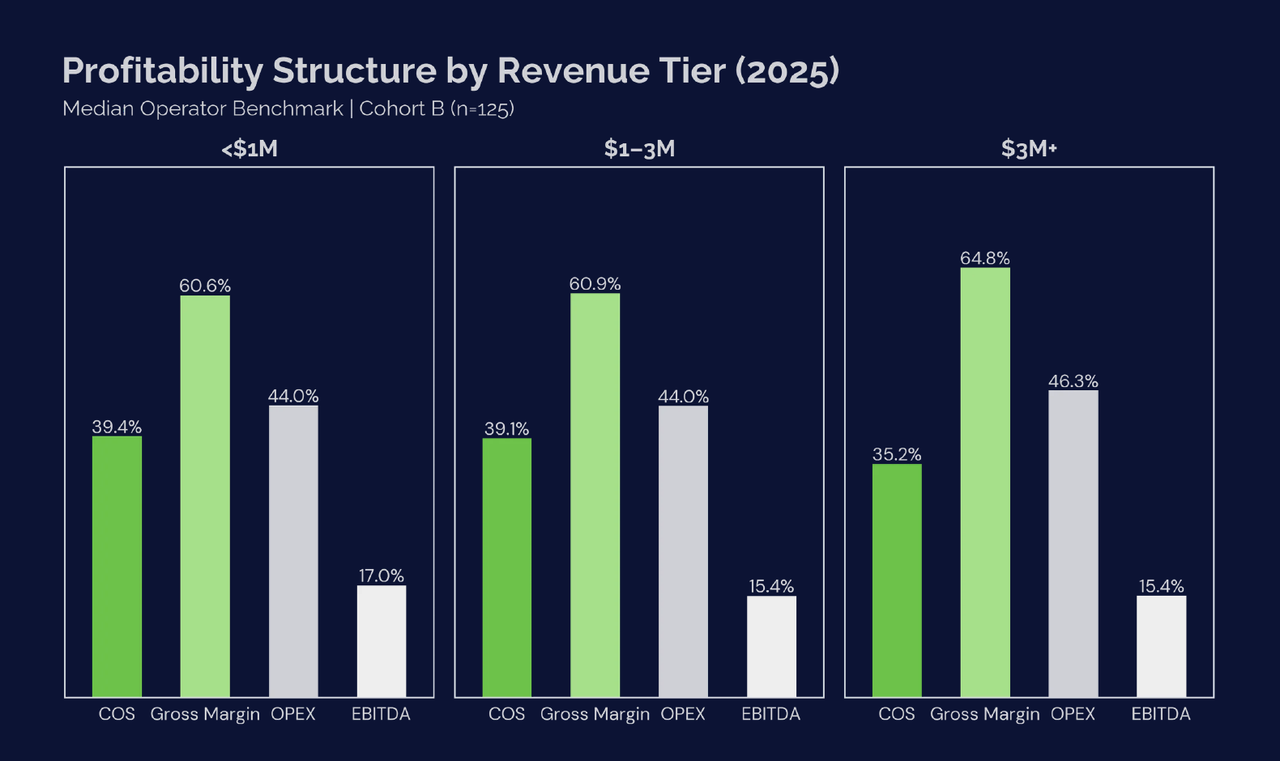

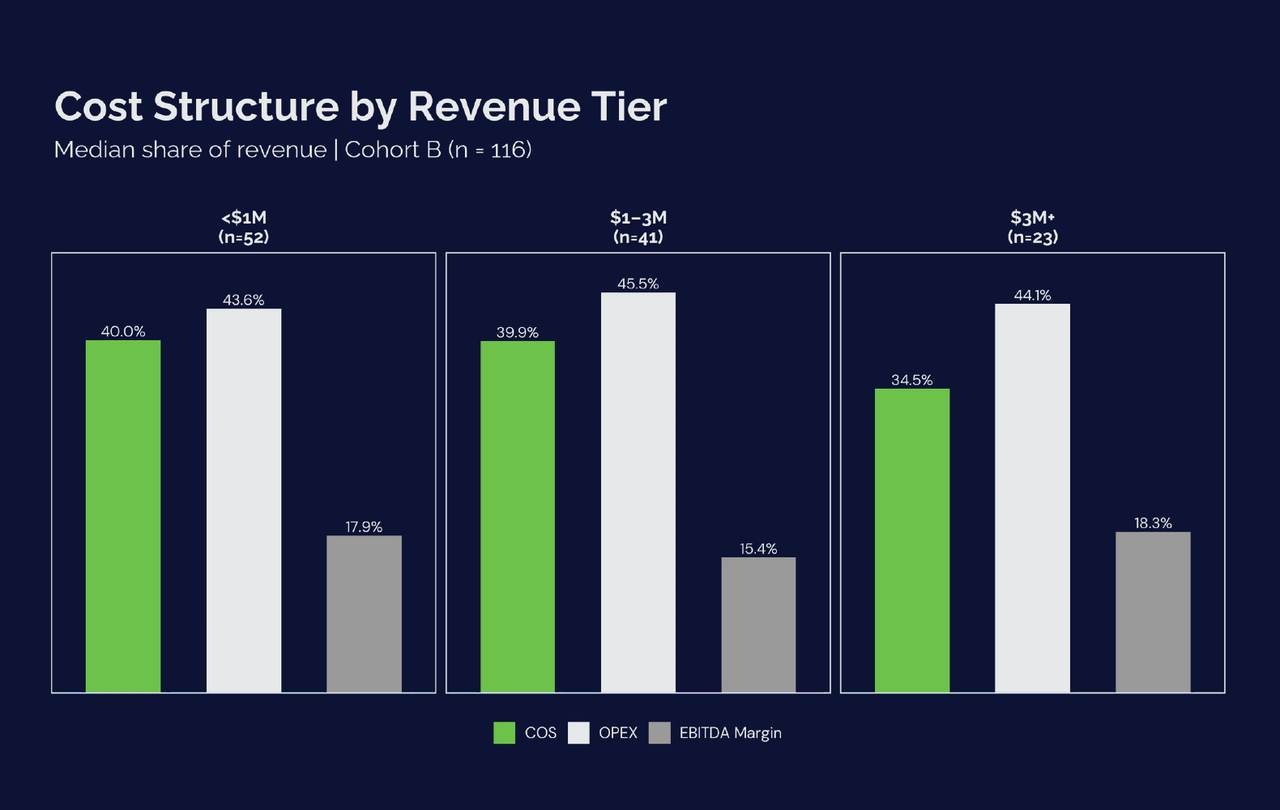

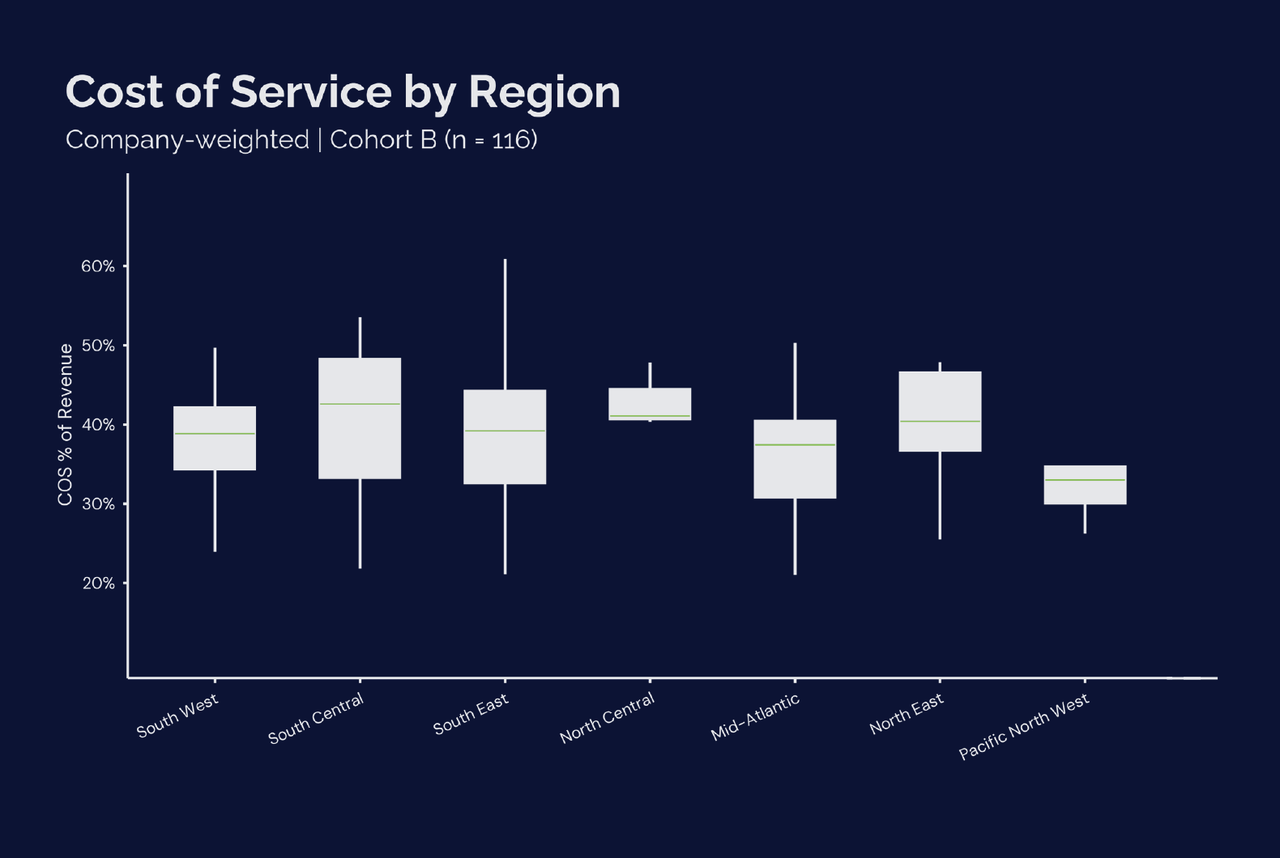

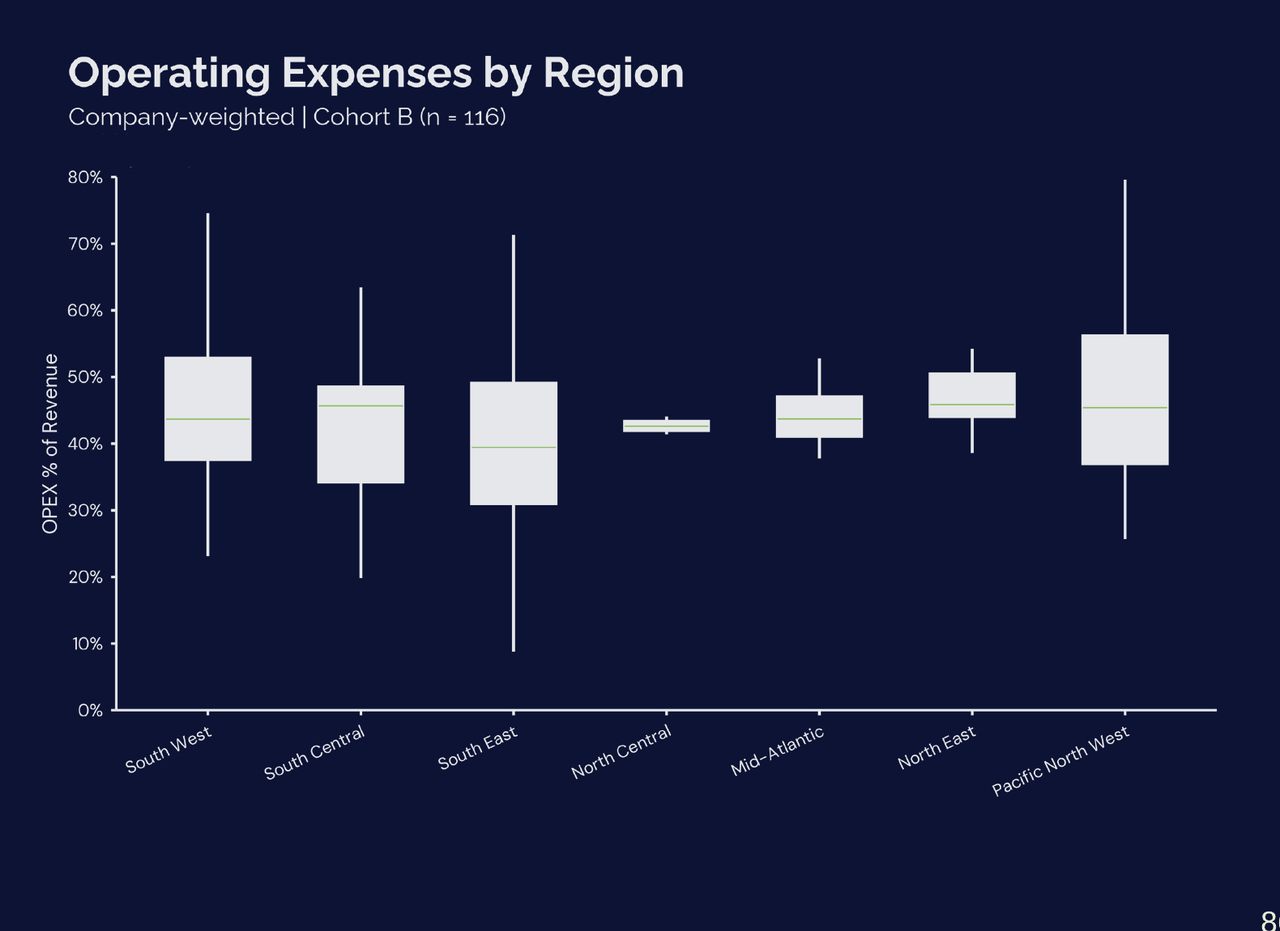

6.3 Cost Structure by Revenue Tier (2024–2025)

Cost structure varies meaningfully by company scale. Examining expense ratios and EBITDA Margin across revenue tiers highlights how operational complexity and scale influence the balance between field delivery costs and overhead.

| 2024 Revenue Tier | COS | OPEX | Margin |

|---|---|---|---|

| <$1M | 40.0% | 43.6% | 17.9% |

| $1–3M | 39.9% | 45.5% | 15.4% |

| $3M+ | 34.5% | 44.1% | 18.3% |

Several structural patterns emerge across the revenue groups. Larger operators ($3M+) tend to operate with lower Cost of Service ratios, reflecting stronger route density, improved technician utilization, and more developed operational systems. However, these efficiencies are partially offset by the higher overhead required to support larger organizational structures.

Notably, the $1–3M tier exhibits the lowest median EBITDA Margin, indicating that companies in this range often experience a transitional phase where organizational complexity begins to increase faster than operational efficiency.

These patterns illustrate how cost structures evolve as companies scale. Operators generating less than $1M in revenue typically operate with lean administrative structures and rely more heavily on owner-operators or small technician teams. As a result, a larger share of revenue is often allocated to direct service delivery costs.

Companies in the $1–3M tier often begin adding operational infrastructure, including dispatch functions, office staff, and expanded technician teams. These additions increase operating overhead but also support greater service capacity and growth potential.

At the $3M+ level, organizations typically introduce more formal management layers, sales infrastructure, and administrative support. While these additions increase overhead, larger operators often benefit from improved route density, stronger pricing discipline, and greater operating leverage.

These dynamics point to a clear operational implication: as businesses scale, the challenge is not simply adding capacity but ensuring that each layer of overhead is introduced in line with measurable gains in productivity. In practice, this means actively managing technician utilization, monitoring revenue per employee, and aligning support functions to field output, rather than allowing overhead to expand ahead of operational needs.

6.4 Expense Scaling Patterns (2024–2025)

Despite strong Revenue Growth across the cohort, bottom-line profitability outcomes were mixed. Median EBITDA Margin increased by only +0.24 percentage points, indicating that revenue expansion and cost growth moved largely in tandem for a typical operator. In other words, the industry did not experience a meaningful marginal improvement in profitability during the period.